Table of Contents

Before buying, looking for the differences between life Insurance vs health insurance? Please note that be it the purpose, beneficiary or the tenure, both of them are entirely different.

Also, if you are curious to know more about the differences between life insurance and health insurance, read this blog till the end.

Key Takeaways

- Purpose: Life insurance is meant for financial protection after death while health insurance is for medical expenses during your lifetime.

- Beneficiary: Life insurance pays the family/nominees whereas health insurance pays the hospital or the policyholder.

- Tenure: Life insurance is usually long-term i.e. 10–40 years while health insurance is usually an annual contract renewed every year.

- Tax Benefits: Life insurance falls under Section 80C and health insurance falls under Section 80D.

- Survival Benefit: Some life insurance plans offer money back if you survive whereas health insurance only provides cover for treatment costs.

Join our Online Course and Learn Stock Marketing the Right Way. Enrol Now!

Introduction

1: What is a stock?

In India, we often use the word “insurance” as a broad term, but mixing up Life Insurance vs Health Insurance can be a costly mistake in your financial journey. Imagine a situation where you have a solid life cover but no health cover.

If a medical emergency happens, you might have to dip into your life’s savings. Or you might even have to sell your assets to pay the hospital bills. On the other hand, if you have only health insurance but no life cover, your family could face a severe financial crisis in your absence.

The first step toward a secure future is to have a proper understanding of the fundamental Life Insurance vs Health Insurance differences. One acts as a safety net for your family’s tomorrow, while the other acts as a shield for your health today.

More about Life Insurance

Life Insurance, in simple terms, is a contract between you and an insurance provider. Here you pay a specific amount known as premium. In exchange, the insurer promises to pay a large sum of money called ‘Sum Assured’ to your family in case something unfortunate happens to you.

The primary goal here is income replacement. Life insurance offers you the guarantee that your children’s education, your spouse’s lifestyle, and any outstanding loans like a home loan are taken care of even if you pass away. Believe it or not, the life insurance coverage in rural India stands at a mere 8-10%.

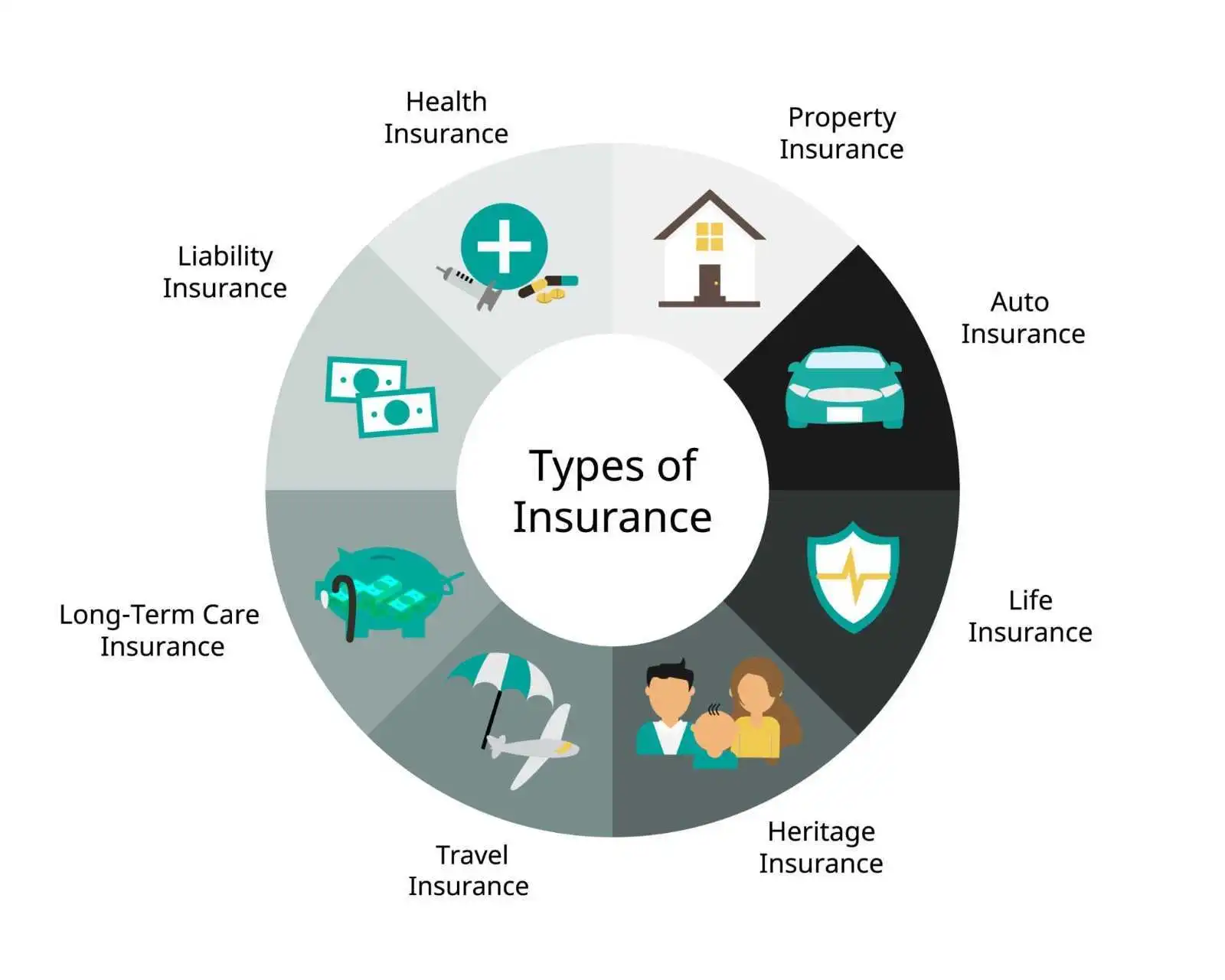

Common Types of Life Insurance in India

- Term Insurance: The simplest and cheapest form. It provides high coverage for a specific period but offers no money back if you survive the term. A study shows that though 74% of people are aware of term plan products, only 34% of them actually own this cover.

- Endowment Plans: They combine insurance with savings and here you get a lump sum if you survive the policy term.

- ULIPs (Unit Linked Insurance Plans): Here a part of your premium goes toward insurance, and the other part is invested in the stock market.

- Whole Life Insurance: This covers you until the age of 99 or 100, providing a legacy for your heirs.

More about Health Insurance

Health Insurance, often known as ‘Mediclaim’ in India, is designed to cover the costs of medical treatment. As the cost of private healthcare in India is skyrocketing, a single hospital stay can wipe out months of savings. The sad part is that only around 39-48% of Indian households have any kind of health insurance coverage.

With health insurance, policyholders are ensured that the insurance company meets the expenses related to hospitalisation, surgeries, doctor consultations, and medicines.

4 Common Types of Health Insurance in India

| 1. Individual Health Insurance | This policy covers a single person. |

| 2. Family Floater | One policy covers the entire family i.e. spouse, children, and sometimes parents under a single sum insured. |

| 3. Critical Illness Cover | Provides a lump sum if you are diagnosed with a specific major illness like cancer or kidney failure. |

| 4. Senior Citizen Health Insurance | Specially designed for those above 60 years of age. |

Detailed Comparison : Life Insurance vs Health Insurance

To truly grasp the Life Insurance vs Health Insurance debate, we need to look at specific parameters that set them apart.

1. The Core Objective

The main objective of life insurance is to provide a financial cushion to your dependents after your death. It is about “what happens after me.”

On the other hand, health insurance is about “what happens to me now.” It covers the cost of getting better when you fall ill or meet with an accident. It is to be noted that during the period between 2017 and 2024, it was India that clocked the steepest rise in financial stress from out-of-pocket (OOP) healthcare spending among 12 Asian markets, reveals a report by Swiss Re.

2. Payment of Benefits

In a Life Insurance policy, the “Death Benefit” is paid out as a lump sum to your nominees. In some plans (like endowment or money-back), you also get “Maturity Benefits” if you outlive the policy.

In Health Insurance, the benefit is usually “Indemnity-based.” This means the company pays the actual hospital bill (up to the sum insured). If your bill is ₹2 lakhs and your cover is ₹5 lakhs, the company pays ₹2 lakhs. You don’t get the remaining ₹3 lakhs as a “profit.”

3. Policy Duration (Tenure)

Life insurance is a long-term commitment. People usually buy it for 20, 30, or even 40 years. You lock in a premium at a young age, and it typically stays the same throughout.

Health insurance is usually a one-year contract. You must renew it every year. The premiums in health insurance often increase as you get older because the risk of falling ill increases with age.

4. Tax Benefits under the Income Tax Act

This is a favourite topic for Indian taxpayers.

- The premiums paid for life insurance are eligible for deduction under Section 80C i.e. up to ₹1.5 lakh per year. Also, the pay-out received by the nominee is generally tax-free under Section 10(10D).

- The premiumspaid for health insurance are eligible for deduction under Section 80D. Also, you can claim up to ₹25,000 for yourself/family and an additional ₹25,000 to ₹50,000 for your parents, depending on their age.

| Feature | Life Insurance | Health Insurance |

| Primary Goal | Financial security for family | Coverage for medical bills |

| When it pays | Death or Maturity | Hospitalization or Illness |

| Who gets money | Nominees/Beneficiaries | Hospital or Policyholder |

| Tenure | Long-term (Years/Decades) | Short-term (Renewed annually) |

| Tax Section | Section 80C | Section 80D |

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

Know moreWhy You Need Both

Most of the people are confused about whether to buy life insurance or health insurance. However, it is better to realise at least now that they are not substitutes for each other.

Comparing Life Insurance vs Health Insurance is equivalent to comparing a helmet to a seatbelt. The truth is that depending on the vehicle and the situation, you need both.

- The Medical Debt Trap: In India, medical inflation is rising at 14–15% annually. If you don’t have health insurance, a major surgery could lead you to debt.

- The Loss of Income: If the main earning member of a family passes away, life insurance ensures that the family doesn’t have to compromise on their dreams or basic needs.

3 Top Factors To Consider

For Life Insurance:

- Human Life Value: Calculate how much money your family would need to replace your income. A thumb rule is 10–15 times your annual income.

- Claim Settlement Ratio (CSR): Always check the CSR of the company as it tells you how many claims the company has settled out of every 100 claims received.

- Riders: You can add “Health Riders” to a life policy, like a Critical Illness rider, to get some health-related benefits.

For Health Insurance:

- Network Hospitals: See if your preferred local hospitals feature on the list of cashless hospitals of the insurer.

- Waiting Period: Almost all health plans have a waiting period of usually 2–4 years for pre-existing diseases like diabetes or hypertension.

- Co-payment: There are some policies that require you to pay a percentage of the bill (e.g., 10%) yourself. Try to choose policies with “No Co-pay.”

Join our Online Course and Learn Stock Marketing the Right Way. Enrol Now!

Conclusion

To sum it up, the Life Insurance vs Health Insurance differences depend upon the type of risk you are covering. Life insurance covers the risk of dying an early death whereas health insurance covers the risk of medical expenses during life.

From the Indian context, if you are looking for a comprehensive financial plan, start by getting a basic health Insurance like Family Floater to protect your savings. In addition to that, buy a Term Life Insurance policy as well to protect your family’s future.

With both in place, ensure that neither a hospital bill nor an unexpected tragedy spoils your family’s financial stability.

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

Know moreFrequently Asked Questions

Can I have a single policy for both?

Yes, some “Combi-plans” offer both, or you can add a health rider to your life insurance. However, separate policies usually offer better, more specialized coverage.

Does life insurance cover hospital bills?

Generally, they don’t. Pure life insurance only pays upon death, but if you have a ‘Critical Illness Rider,’ you might get a lump sum upon diagnosis.

Is health insurance premium fixed for life?

No. Health insurance premiums will usually increase every few years as you move into higher age brackets or due to medical inflation.

What happens if I don't claim my health insurance?

Most Indian insurance companies offer a ‘No Claim Bonus’ (NCB), which either increases your sum insured or gives you a discount on the next year’s premium.

Can I buy life insurance for my kids?

You can buy “Child Plans” for their future goals (education), but “Term Insurance” is usually meant for earning members to replace lost income.

Does health insurance cover death?

No. Health insurance only covers medical expenses and it does not provide any financial compensation to the family in the event of the policyholder’s death.

Are both mandatory in India?

Neither is mandatory by law (unlike third-party motor insurance), but both are essential for financial survival in today’s world.

{kind=link}