Table of Contents

Starting a new business is thrilling, but financing control may be considered one of the biggest demanding situations for startups. Many marketers, mainly without background in accounting, often make errors which could purpose critical economic issues. These mistakes may appearance shorter before everything, but can boom in primary problems over time if they’re not handled properly.

In this blog, we will highlight the start -up of the most common accounting errors and share simple, practical suggestions to avoid them. Whether you start now or want to improve financial management, understanding these disadvantages can help you create a strong base for your business.

Become an Accounting Pro – Learn from Industry Experts!

Top Accounting Mistakes Startups Make

How to Avoid These Accounting Mistakes

Avoiding common accounting mistakes can save startups from serious financial trouble and set a strong foundation for sustainable growth. Here are some practical ways to steer clear of these pitfalls:

🔷 Use Reliable Accounting Software

Invest in user -friendly accounting software such as QuickBooks, Xero, FreshBooks or Zoho Books. These devices help you to be organized to automate financial functions, track income and expenses, generate reports and reduce the opportunities for manual errors.

Choosing the right accounting software can make or break your financial workflow. Good software doesn’t just crunch numbers—it helps you stay organized, save time, and reduce costly errors. With features like automated invoicing, expense tracking, bank syncing, and real-time reporting, it takes the guesswork out of managing your money. Plus, it scales with your business as you grow. Whether you’re a solo founder or building a team, using reliable accounting software gives you a clear view of your finances—and peace of mind.

🔷 Separate Business and Personal Finances

Open a dedicated business bank account and get a business credit card. To maintain clarity and avoid legal or tax issues, keep all business -related expenses and income separated from personal finance.

Mixing business and personal finances is a recipe for confusion—and potential tax trouble. Keeping them separate helps you track expenses clearly, stay organized, and make smarter financial decisions. Open a dedicated business bank account, use a business credit card, and always log business transactions independently. Not only does this make bookkeeping easier, but it also shows professionalism and builds credibility with investors, lenders, and the IRS. Think of it as drawing a clean line between your hustle and your home life.

🔷 Track Every Expense

Register each financial transaction – no matter how small. Use a mobile app or receipt scanner to capture the receipts. Classify expenses to monitor expenditure habits and identify unnecessary costs.

Every dollar counts—literally. Tracking every expense helps you understand where your money is going, catch unnecessary spending, and stay prepared for tax time. Whether it’s a software subscription, a coffee with a client, or a last-minute office supply run, logging each cost keeps your books accurate and up to date. Use accounting software or even a mobile app to snap receipts and categorize expenses in real time. Staying on top of this habit means fewer surprises and smarter budgeting down the road.

🔷 Plan and Monitor Cash Flow

Make a monthly cash flow forecast and update it regularly. Monitor how you have enough money for necessary operations and unexpected costs to ensure how the money goes into your business and outside.

Cash flow is the lifeblood of any business. Without a clear picture of what’s coming in and going out, even profitable companies can run into trouble. Planning and monitoring your cash flow means forecasting expenses, anticipating income, and making sure you always have enough on hand to cover the essentials. It helps you avoid late payments, seize growth opportunities, and sleep a little easier at night. Staying proactive—not reactive—with your cash flow can make all the difference between surviving and thriving.

🔷 Set Aside Money for Taxes

Always save a portion of your earnings for taxes. Create a tax savings account and deposit a set percentage of your income each month. This helps avoid last-minute panic and penalties.

Taxes can sneak up fast if you’re not prepared. Setting aside money throughout the year helps you avoid the last-minute scramble—and the stress that comes with it. A good rule of thumb is to save a percentage of every payment you receive, based on your expected tax rate. Keep it in a separate account so it’s out of sight, out of mind. When tax season rolls around, you’ll be ready to pay what you owe without disrupting your cash flow. Future-you will thank you.

🔷 Hire a Professional When Needed

Always save some of your tax revenue. Create a tax savings account and deposit a fixed percentage of income each month. It helps to avoid nervousness and punishment at the last minute.

Sometimes, the smartest money move is knowing when to call in the pros. As your business grows, your finances can get more complex—think payroll, taxes, compliance, or scaling strategies. A qualified accountant or financial advisor can help you avoid costly mistakes, maximize deductions, and plan for the future. It’s not a sign of weakness—it’s a sign you’re serious about doing things right. Investing in expert help can save time, reduce stress, and give you the confidence to focus on what you do best.

🔷 Review Financial Reports Regularly

Check financial reports such as income statements, balance sheets, and cash flow statements monthly. These reports help you understand your business’s financial health and make informed decisions.

Your financial reports are like a health checkup for your business. Reviewing them regularly—monthly, quarterly, or even weekly—helps you catch red flags early, spot trends, and make smarter decisions. Keep an eye on your profit and loss statement, balance sheet, and cash flow report to understand how your business is really performing. It’s not just about the numbers; it’s about the story they tell. When you stay informed, you’re better equipped to steer your business with confidence and clarity.

🔷 Create a Budget and Stick to It

Make a realistic monthly or quarterly budget to manage expenses effectively. Budgets help control spending, allocate resources wisely, and support strategic decision-making.

A budget isn’t just a spreadsheet—it’s your financial game plan. Creating a clear, realistic budget helps you manage spending, prioritize investments, and stay on track with your goals. It sets limits, keeps surprises to a minimum, and gives you a sense of control over your finances. The key is sticking to it. Review it often, adjust when needed, and treat it as a living tool, not a one-time task. When you budget with intention, every dollar has a purpose—and that’s powerful.

🔷 Schedule Regular Financial Check-ins

Determine weekly or monthly time to review your finances. This habit helps to catch anomalies quickly, remain organized and make better decisions on business growth and money.

Running a business is busy, but taking time to review your finances regularly is non-negotiable. Scheduling weekly or monthly financial check-ins helps you stay informed, spot potential issues early, and make timely decisions. Whether you’re doing it solo or with your accountant, these sessions keep your goals aligned with your actual performance. It’s like hitting pause to make sure you’re still on the right path. Consistent check-ins turn finances from a guessing game into a guided strategy.

🔷 Educate Yourself

Learn basic accounting principles through online courses, webinars or training programs. Even if you appoint a professional, it helps to have a basic understanding of your financing clearly communicating and making smart options.

Even if you hire a professional, having a basic understanding of accounting can go a long way. Learning the fundamentals—like how to read financial statements or understand cash flow—helps you make smarter decisions and communicate more clearly with your accountant. You don’t need a finance degree; online courses, webinars, or training programs can teach you the essentials at your own pace. The more financially literate you are, the more confident you’ll feel steering your business forward.

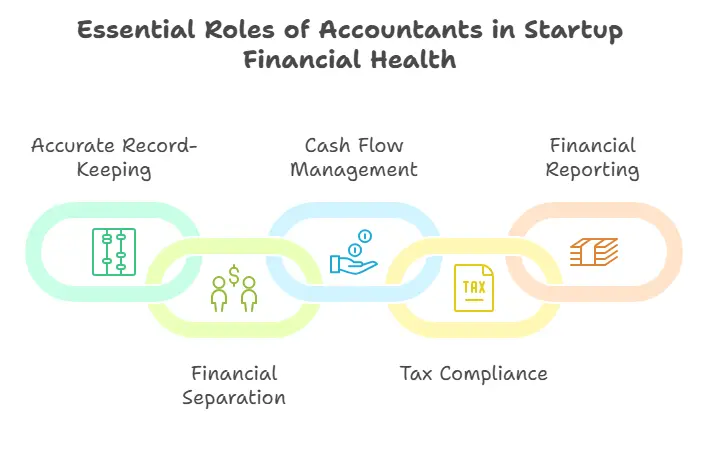

The Role of Accountants in Preventing Accounting Mistakes

Accountants play an important role in helping startups to maintain financial health and to avoid general accounting losses. Their expertise is just outside the balance between books-they provides strategic insights, ensures compliance and supports long-term development. This is how accountants help prevent expensive accounting errors:

✅ Ensuring Accurate Record-Keeping

Professional accountants maintain detailed and accurate financial records. They ensure that each transaction is properly recorded and classified correctly, which reduces the possibility of errors and improves financial transparency.

Accurate record-keeping is essential for any organization to ensure compliance, facilitate smooth operations, and provide transparency. Properly maintained records help in decision-making, auditing, and tracking progress. In this section, we’ll explore key practices to ensure your record-keeping is precise and reliable.

1. Implement a Consistent System

Having a clear and structured system for storing records is crucial. Whether digital or physical, the system should be easy to navigate and standardized. This allows team members to access and update records efficiently, ensuring consistency and accuracy across the board.

2. Regular Audits and Reviews

Regular audits of the records are essential to verify their accuracy. This can be done on a monthly or quarterly basis depending on the volume of records. Auditing helps identify discrepancies, outdated information, or gaps that need to be addressed promptly.

3. Proper Training for Staff

Staff members responsible for record-keeping should be trained on best practices and the importance of accuracy. Training ensures that everyone follows the same protocols and understands the implications of mishandling records, reducing the risk of errors.

4. Utilize Technology for Automation

Technology can streamline record-keeping processes. By using software for data entry, storage, and retrieval, the chance of human error is minimized. Automated backups also ensure that records are safe and can be recovered in case of data loss.

5. Ensure Legal Compliance

Record-keeping must comply with industry regulations and legal requirements. Different types of records may have specific retention periods, and failing to adhere to these guidelines can lead to penalties or legal issues.

✅ Helping Separate Business and Personal Finances

Accountants guide business owners in establishing separate accounts and installing clear boundaries between individual and business transactions. This is important for tax reporting, auditing and general clarity in financial management.

Separating business and personal finances is a critical step for entrepreneurs, freelancers, and small business owners. It not only simplifies financial management but also provides clarity, ensures legal protection, and enhances the credibility of the business. Here’s how to achieve and maintain a clear distinction between the two.

1. Open a Dedicated Business Bank Account

One of the first steps is to open a separate bank account exclusively for business transactions. This helps in tracking income and expenses accurately, avoiding confusion during tax filing, and maintaining a professional image with clients and vendors.

2. Use Business Credit Cards

Using a business credit card for all company-related expenses is another smart move. It allows you to build business credit, manage cash flow more effectively, and easily categorize expenditures without mixing them with personal purchases.

3. Pay Yourself a Salary or Draw

Instead of dipping into business funds at random, establish a method for paying yourself. Whether it’s a fixed salary or a regular owner’s draw, this approach promotes discipline and ensures you’re not treating the business account like a personal wallet.

4. Keep Accurate Records

Maintaining detailed records of both business income and expenses is essential. It helps avoid accidental cross-over between personal and business finances and serves as a valuable resource during audits, loan applications, or tax season.

5. Create a Budget and Stick to It

Develop separate budgets for personal and business use. This helps in planning, prevents overspending, and ensures that each entity operates within its financial limits.

6. Avoid Cash Transactions

Cash transactions can make it harder to track business expenses and prove them if needed. Using traceable methods like checks, cards, or digital payments makes it easier to maintain a clear financial trail.

✅ Monitoring Cash Flow Efficiently

Cash flow problems are one of the main causes that fail. Accountants track revenues and expenses regularly, identify cash flow gaps and offer strategies to manage money more efficiently to avoid getting out of money.

Efficient cash flow monitoring is the backbone of a financially healthy business. It enables organizations to maintain solvency, make informed decisions, and prepare for future growth. Proper cash flow management ensures that a business has enough liquidity to meet its obligations while also investing in opportunities.

1. Understand Cash Inflows and Outflows

Start by clearly identifying all sources of cash inflow (e.g., sales, loans, investments) and cash outflow (e.g., rent, salaries, inventory purchases). Knowing where money is coming from and where it is going is essential to maintain a clear financial picture.

2. Use Cash Flow Statements

Regularly prepare and review cash flow statements to track the movement of cash within your business. This document categorizes cash activities into operations, investing, and financing, providing a snapshot of your financial health at any given time.

3. Implement Accounting Software

Using accounting software automates cash flow tracking, generates real-time reports, and reduces human error. Tools like QuickBooks, Zoho Books, or Xero can help you visualize trends and set alerts for low cash levels.

4. Forecast Future Cash Flow

Develop short-term and long-term cash flow forecasts to anticipate upcoming expenses and income. Forecasting allows businesses to plan ahead, avoid shortages, and take advantage of growth opportunities without risking liquidity.

5. Maintain a Cash Reserve

A dedicated cash reserve helps handle unexpected expenses such as repairs, slow sales periods, or emergency purchases. Having a buffer ensures that the business remains stable even during tough times.

✅ Managing Tax Obligations

Tax rules can be complicated, and wrong to bring the missing time limit or income can lead to punishment. Accountants help start up to understand their tax obligations, calculate the obligations accurately and file returns in time.

Effective management of tax obligations is crucial for any business or individual to remain compliant with the law while optimizing their financial resources. By staying organized, understanding your tax responsibilities, and utilizing strategies to minimize liabilities, you can ensure smooth operations and avoid penalties.

1. Understand Tax Obligations

The first step is to have a clear understanding of the taxes you are required to pay, including income tax, sales tax, payroll tax, and other local, state, or federal taxes. Consult with a tax professional to ensure you know what applies to your business or personal finances.

2. Keep Accurate Records

Accurate and up-to-date record-keeping is essential for managing tax obligations effectively. Keep track of all receipts, invoices, and financial transactions. Proper documentation makes it easier to file tax returns, claim deductions, and defend against any audits.

3. Set Aside Funds for Taxes

It’s important to set aside a portion of your income or business revenue specifically for tax purposes. This will help avoid cash flow problems when tax season arrives. Estimate your tax liability and reserve the necessary amount to pay on time.

4. Use Tax Software or Professionals

Tax software can simplify the process of filing taxes by automating calculations and ensuring you’re applying the correct tax rules. Alternatively, hiring a professional accountant or tax advisor can ensure accuracy, provide advice on tax-saving strategies, and help you navigate complex tax laws.

5. Stay on Top of Deadlines

Missing tax deadlines can result in fines and penalties. Mark important tax filing dates on your calendar or set reminders. Depending on your situation, you may also need to make estimated tax payments throughout the year.

6. Take Advantage of Deductions and Credits

Make sure to identify all available deductions and credits that apply to your business or personal finances. These can significantly reduce your tax burden. For businesses, this could include deductions for business expenses like office supplies or home office costs. For individuals, credits for education, healthcare, or charitable donations may apply.

✅ Generating and Analyzing Financial Reports

Accountants prepare necessary financial reports such as income details, balance sheet and cash flow accounts. They also interpret these reports to get business owners to make smart decisions and to help plans for the future.

1. Identify Key Financial Reports

The most common financial reports include:

-

Income Statement (Profit & Loss Statement): Shows the company’s revenue, expenses, and profits over a specific period.

-

Balance Sheet: Provides a snapshot of the company’s assets, liabilities, and equity at a particular point in time.

-

Cash Flow Statement: Tracks the flow of cash in and out of the business, indicating liquidity and cash management.

-

Statement of Shareholder Equity: Shows changes in the ownership interest of the company’s shareholders.

2. Use Accounting Software

Modern accounting software like QuickBooks, Xero, or FreshBooks can automate the process of generating financial reports. These tools not only make the process faster and more accurate but also allow for real-time data entry, making it easier to track financial performance consistently.

3. Ensure Accuracy in Data Entry

Accurate financial reports are built on correct data. It’s essential to have a structured system for recording financial transactions. Regular audits and reconciliations of accounts can help eliminate errors and ensure the accuracy of financial reports.

4. Monitor Key Performance Indicators (KPIs)

While generating financial reports, it’s important to track KPIs that are specific to your business objectives. Common financial KPIs include:

-

Gross Profit Margin

-

Net Profit Margin

-

Current Ratio

-

Return on Assets (ROA)

-

Accounts Receivable Turnover

Analyzing these KPIs helps in assessing the financial health and operational efficiency of the business.

5. Compare Reports with Historical Data

To gain a deeper understanding of financial performance, compare current reports with past data. This comparison can help identify trends, such as revenue growth or cost reductions, and highlight areas that need attention.

✅ Providing Budgeting and Forecasting Guidance

Accountants help create realistic budget and financial forecasts. The scheme helps to assign the start -ups intelligently, control costs and determine the goals achieved based on data -driven estimates.

Budgeting and forecasting are essential financial planning tools that help individuals and businesses allocate resources wisely, anticipate future needs, and stay on track with their financial goals. These practices provide clarity, reduce uncertainty, and support better decision-making by offering a financial roadmap for both the short and long term.

1. Establish Clear Financial Goals

Start by defining your short-term and long-term financial goals. These could include increasing revenue, reducing debt, expanding operations, or saving for a major purchase. Having specific objectives helps shape your budget and forecasts with purpose and direction.

2. Create a Realistic Budget

A budget outlines expected income and expenses over a specific period—monthly, quarterly, or annually. To create an effective budget:

-

Review historical financial data.

-

Categorize fixed and variable expenses.

-

Prioritize essential spending.

-

Allocate funds for savings or investment.

A realistic budget serves as a daily financial guide and helps control overspending.

3. Analyze Past Performance

Use historical financial reports to identify trends and inform your forecasting. Understanding past income, costs, and seasonal patterns helps make more accurate predictions about future financial performance.

4. Use Forecasting Tools and Techniques

Forecasting involves predicting future revenues, expenses, and cash flows based on current and past data. Techniques include:

-

Trend Analysis: Identifies patterns from historical data.

-

Moving Averages: Smooths fluctuations to see long-term trends.

-

Scenario Planning: Models best-case, worst-case, and most likely financial outcomes.

Modern forecasting software can also automate calculations and provide dynamic visualizations.

5. Regularly Monitor and Update

Budgets and forecasts should be living documents—regularly reviewed and updated based on actual performance and changing conditions. This allows for timely adjustments and helps stay aligned with financial goals.

✅ Identifying and Correcting Errors Early

With regular revision and reconciliation, accountants can quickly see anomalies or unusual activity. Initial detection helps prevent small errors from becoming major financial problems.

Identifying and correcting financial errors early is vital to maintaining accuracy, ensuring compliance, and preventing small mistakes from escalating into major issues. Early detection helps preserve the integrity of financial records and supports informed decision-making.

1. Implement Regular Reconciliation

Regularly reconcile your financial statements—such as comparing bank statements with accounting records—to spot discrepancies quickly. This helps ensure all transactions are accounted for and accurately recorded.

2. Use Automated Accounting Software

Modern accounting tools often include built-in error detection features. They can flag inconsistencies, duplicate entries, or out-of-balance accounts, making it easier to catch issues early on.

3. Establish Internal Controls

Set up clear internal procedures, such as requiring approvals for expenditures, separating duties among staff, and conducting regular audits. These controls reduce the risk of both accidental errors and fraudulent activity.

4. Conduct Periodic Reviews

Schedule routine reviews of your financial documents, including ledgers, invoices, and receipts. Having a second set of eyes—either a colleague or accountant—can help uncover errors that might go unnoticed.

5. Train Staff on Best Practices

Ensure that employees involved in financial tasks are well-trained on data entry, record-keeping, and software use. Proper training minimizes human errors and promotes consistency in financial operations.

6. Monitor for Red Flags

Stay alert to common warning signs, such as unexplained account balances, sudden cash flow changes, or mismatched financial reports. Investigating these early can lead to timely corrections and prevent further complications.

7. Document and Correct Promptly

Once an error is identified, document the nature and cause of the error and take immediate steps to correct it. Make the necessary adjustments in your records and clearly note why the correction was made.

Become an Accounting Pro – Learn from Industry Experts!

Conclusion

1: Accounting provides information on

Accounting errors can be an important path for success and life for a start -up. Failure to track expenses to neglect tax obligations can lead to financial instability, lost opportunities and even legal issues. However, with proper planning, proper equipment and professional guidance, these losses can be easily avoided.

Entrepreneurs can ensure their business evenly, by implementing accurate record keeping, separating business and personal finance and reviewing regular financial reports. To put separate funds for tax, manage cash flow effectively and seek help from professionals when needed, and promote the start -ups from expensive errors.

| Related Links | |

|

How to Choose the Right Accounting Structure for Your Startup |

|

Placement Oriented PWC Business Accounting Course

PWC Certified Business Accounting Course by Entri App: Master in-demand skills, ace interviews, and secure top-tier jobs.

Join Now!Frequently Asked Questions

Why is it important for startups to avoid accounting mistakes?

Accounting mistakes can lead to coins float troubles, incorrect monetary reporting, lost tax deadline or even felony issues. Avoiding these errors facilitates to make certain monetary stability and construct believe with traders and stakeholders.

What are the most common accounting mistakes startups make?

Some of the most common errors include mixing individual and professional economy, leading bad records, ignoring taxes and failing to use the right accounting software.

How can startups prevent accounting errors without hiring a full-time accountant?

Start -up can use reliable accounting software, can take basic accounting courses, keep accurate items and plan regular financial assessments. They can also outsource for participants or accounting services as needed.

When should a startup hire a professional accountant?

It is best to appoint a professional when the business begins to generate regular revenue, tax preparations, apply for money, or when financial functions become very complicated to manage internally.

{kind=link}