Table of Contents

Being a freelancer, this particular question must have found its way into your brain:

Do I have to pay taxes?

Well, there is only one answer, and that is yes! Regardless of not getting a paycheck every month, the government considers you a tax-paying citizen. So, is there any difference in filing an ITR if I’m a freelancer? If so, how do I file the ITR? This blog provides you with answers on how to file ITR for freelancers, tax-free!😉

Check out this video by Entri in Malayalam!

Key Takeaways:

- Freelancers = self-employed = need to pay tax

- You need to track all your income and expenses for ITR filing.

- You can deduct the expenses as they are for your professional cause.

- File ITR-4 or ITR-3 based on how your income is categorised.

- Consider advance tax if your income is high, and the self-assessment fee, if applicable.

Introduction: Do Freelancers Pay Taxes in India?

Let’s face it, freelancers may not have work around the month as it is solely based on the projects they sign up for. When compared to salaried individuals, even the payments can be somewhat erratic due to a certain level of uncertainty. Therefore, it’s only natural for one to assume that taxes and ITR filing do not apply to the humble yet impactful freelancers. However, that is not the case.

In 2026, 15M+ freelancers face new slabs and ITR-4 tweaks. If you have taken on freelance gigs, such as content writing, design, coding, consulting, or photography, you are considered self-employed. Though that’s not the case, the government finds freelancers as gaining “Income from Business or Profession” and thus makes them eligible for tax. To put it in simple terms, the government sees you as a one-person business similar to a small shop owner.

According to the recent update, individuals with an income of up to 12 lakhs do not need to pay any taxes under the new regime for the financial year 25-26.

So, what income counts?

To put it simply, any income that you gain from doing freelance work is considered income that can make you eligible to pay taxes. This includes:

- Payments received from Indian/foreign clients

- Gigs and income from projects taken up through various platforms like Upwork, Fiverr, Behance, etc.

- Money credited to your bank account, UPI, NEFT, etc.

- Not for commission agents or those needing stock inventory.

- NRIs file ITR-3/4 too, but report global income if RP >182 days.

Remember that if it’s coming into your account, it is counted. This even applies when your employer doesn’t provide you with a Form 16 or any such valid tax forms.

Types of ITR Forms

1: Accounting provides information on

Most people are either unaware or confused about which ITR form they should choose to file. If you choose the wrong form, it may lead to the rejection of the ITR file. Here is a detailed list of the types of ITR forms for individuals to choose from according to their eligibility:

ITR 1

Specifies to salaried individuals, including pensioners and those who have one house property.

ITR 2

Specifies to individuals with capital gains, such as salary, pension, foreign income, interest, dividends, etc. Additionally, the aggregate must be above 50 lakhs in a financial year.

ITR 3

For freelancers maintaining books of accounts or with audit-required income (turnover >₹75 lakh or profit <50% under 44ADA). Includes foreign assets (Schedule FA), crypto (Schedule VDA), and detailed expenses. Use if not eligible for presumptive scheme.

ITR 4 (Sugam)

For presumptive taxation under Section 44ADA (receipts ≤₹50 lakh any mode OR ≤₹75 lakh with ≥95% digital payments like UPI/bank). 2026 updates: Supports 2 house properties, LTCG ≤₹1.25 lakh (u/s 112A), mandatory bank balance disclosure, and Virtual Digital Assets reporting. No books/audit needed.

Note: ITR-4 for most freelancers under 44ADA limits—simplest option. Always check AIS for pre-filled data mismatches.

| Freelancer Type | ITR Form | Limit/Condition |

|---|---|---|

| Presumptive (digital receipts) | ITR-4 | ≤₹75L (95% digital) |

| Books + audit | ITR-3 | >₹75L turnover |

| Crypto/foreign assets | ITR-3 | Any |

| Mixed salary + freelance | ITR-3/ITR-4 | Check AIS |

Placement Oriented PWC Business Accounting Course

PWC Certified Business Accounting Course by Entri App: Master in-demand skills, ace interviews, and secure top-tier jobs.

Join Now!Presumptive Taxation Under Section 44ADA: Ideal for Freelancers

Section 44ADA offers a simple presumptive taxation scheme for professionals like coders, writers, and designers (not traders). You declare 50% of your gross receipts as profit, skipping expense proofs or audits—perfect for freelancers.

Key 2026 Limits

| Payment Mode | Turnover Limit | Deemed Profit |

|---|---|---|

| Any (cash OK) | ₹50 Lakh | 50% |

| ≥95% Digital (UPI/bank) | ₹75 Lakh | 50% |

Essential Rules

- Eligibility: Resident professionals with gross receipts up to the limits.

- Audit Trigger: Required if you declare less than 50% profit or exceed ₹75 Lakh turnover.

- Opt-Out Penalty: Switching to regular taxation bans presumptive scheme for 5 years + mandates audit next year.

- Real Example: ₹60 Lakh from Upwork (98% bank transfers) → Declare ₹30 Lakh as taxable profit → Tax around ₹4 Lakh after rebates.

Easy Step-by-step Guide on How to File ITR for Freelancers

When compared to ITR filing for salaried individuals, the procedure for freelancers is different and may seem a bit difficult. But, with the required documents and by following the detailed step-by-step guide provided below, you can submit your filing as easily as a walk in the park. Read and understand each step to identify which steps apply to you.

Step 1: Calculate Your Income

Your total income earned in a single financial year can be divided into two as a freelancer:

-

Income

This is your main income that you receive from all your clients, including domestic and international. This would be under the “Income from Profession or Business” head, showcasing it as your primary source of livelihood. The parallel incomes that you receive, such as bank interests, FD interests, etc., need to be included under the “Income from Other Sources” section.

-

Expenses

These expenses are those that you have accumulated within the financial year that are allowed as deductions. Maintain records of these expenses to showcase that your:

Net income = Gross receipts – Allowed Business Expenses

The allowed expenses include:

-

Office rent or home-office expenses (partial)

-

Internet, mobile, and electricity bills

-

Travel expenses

-

Hardware/software purchases

-

Depreciation of assets

-

Professional fees (e.g., CA, legal)

-

Subscription to tools/platforms

-

Advertisement or marketing costs

Step 2: Collect the required Documents

-

PAN & Aadhaar card

-

Bank account details

-

Form 26AS

-

AIS (Annual Information Statement) and TIS

-

Invoices issued to clients

-

Expense receipts

-

TDS certificates (Form 16A)

-

Advance tax paid or self-assessment tax challans

What is TDS and TCS? TDS is the Tax deducted at Source, which is paid by you when you receive an income. TCS is Tax Collected at Source, that is, deducted when you buy a product like a house, a car, etc. Both these taxes can be claimed back with ITR filing.

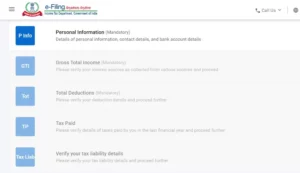

Step 3: Log in to the Portal

Visit https://www.incometax.gov.in/iec/foportal/. Click on the login button or the register button if you are new to this site. You can log in and register using your PAN or Aadhaar. Fill in the required details to get started on ITR filing.

Step 4: Assessment Year and ITR Form

Once you have registered and logged in, you will be required to select the assessment year (25-26), followed by the ITR form (ITR-3 or ITR-4). Choose them accordingly.

Latest Update: Income Tax Return Forms of ITR-1 and ITR-4 are enabled to file through the Online mode with prefilled data at the e-filing portal. Excel Utilities of ITR-1 and ITR-4 for AY 2025-26 are also available for filing.

Step 5: Provide the required details

-

Personal details

-

Nature of business/profession code (e.g., 0701 for software development)

-

Income from profession

-

Expenses (if not under presumptive)

-

Other sources of income

-

Deductions (under 80C, 80D, etc.)

Step 5.5: Key ITR Schedules for Freelancers

Focus on these key schedules in ITR-4 for Section 44ADA filers. Use e-filing portal’s pre-filled data.

Essential Schedules

- Schedule BP: Tick 44ADA → Enter gross receipts only (auto 50% profit).

- Schedule Bank: New: Report balances as on March 31 (pre-filled).

- Schedule TDS: New selector: Import TDS2 from 26AS.

- Schedule VDA: New: Report crypto gains (30% tax).

Tip: Verify AS-26 match to avoid notices.

Step 6: Compute the Tax and Claim Deductions

Compute the total taxable income and apply the eligible deductions (e.g., 80C for LIC/PPF, 80D for medical insurance). Next, compute the final tax liability and check if you have paid excess tax. If so, it will be shown as a refund. Make sure to cross-check the bank details as the refund will be credited to that account.

Step 7: Verify and Submit ITR

Submit the ITR and remember to e-verify within 30 days. You can e-verify using Aadhaar OTP/net banking/DSC. Processing ususally takes from 10 to 45 days.

Additional Steps (if applicable)

These are some of the steps that are additionally applicable based on certain criteria and conditions. Make sure to go through them carefully and proceed with them if any of them is applicable to you.

-

Advance Tax

If tax liability exceeds ₹10,000 in a financial year, pay advance tax quarterly.

Due dates:

-

-

15th June – 15%

-

15th Sept – 45%

-

15th Dec – 75%

-

15th Mar – 100%

-

If you have missed it, you can pay with interest under sections 234B & 234C.

-

Self-assessment Tax

If any tax remains payable after TDS and advance tax, generate a challan (ITNS 280) from TIN NSDL and pay using net banking or UPI.

Also read: How to Save Tax in India – Tax Saving Options and Tips

How Much Tax Do Freelancers Pay in AY 2026-27?

Freelancers in India file taxes under the Income Tax Act, with options for the new tax regime (default and simpler for most) or the old tax regime. Your tax depends on total income after deductions like presumptive profit (e.g., 50% under Section 44ADA). Use ITR-4 for profession income or ITR-3 for business. Here’s a clear breakdown for Assessment Year 2026-27 (FY 2025-26).

New Tax Regime Slabs (Default – Recommended for Simple Filers)

This regime offers lower rates but fewer deductions. It’s ideal for freelancers without heavy expenses. Key benefits include a rebate under Section 87A (up to ₹20,000 if total income ≤ ₹7 Lakh, making tax zero) and a standard deduction of ₹75,000.

| Income Range | Tax Rate | Notes |

|---|---|---|

| ₹0 – ₹4 Lakh | 0% | Completely tax-free. |

| ₹4 – ₹8 Lakh | 5% | Applies to amount over ₹4 Lakh. |

| ₹8 – ₹12 Lakh | 10% | Applies to amount over ₹8 Lakh. |

| ₹12 – ₹16 Lakh | 15% | Applies to amount over ₹12 Lakh. |

| ₹16 – ₹20 Lakh | 20% | Applies to amount over ₹16 Lakh. |

| ₹20 – ₹24 Lakh | 25% | New bracket introduced for 2026. |

| Above ₹24 Lakh | 30% | Plus surcharge (10-37% based on income levels). |

Example: ₹10 Lakh income → Tax = 0 (up to ₹4L) + 5% on ₹4L + 10% on ₹2L = ₹45,000 (before rebate/standard deduction).

Old Tax Regime Slabs (Opt via Form 10-IEA – No Lock-in Now)

Switch to this for more deductions (e.g., HRA, 80C investments). No lock-in period—you can switch yearly. Rates apply progressively.

| Income Range | Tax Rate |

|---|---|

| ₹0 – ₹3 Lakh | 0% |

| ₹3 – ₹7 Lakh | 5% |

| ₹7 – ₹10 Lakh | 10% |

| ₹10 – ₹12 Lakh | 15% |

| ₹12 – ₹15 Lakh | 20% |

| Above ₹15 Lakh | 30% |

Regime Rules for Freelancers

- Profession-only income (use ITR-4): Switch between regimes yearly.

- Business income (use ITR-3): New regime allows one-time switch only.

- Presumptive taxation (44ADA/44AD): Flexible—choose either regime annually.

- Surcharge: Applies on high incomes (>₹50 Lakh); health/education cess at 4%.

- Tip: Calculate both regimes using the ITR portal’s comparator tool for the best fit.

⚠️Important:

Most freelancers overlook the fact that there are some conditions for selecting the regimes. Based on how your income is categorised, you get to choose the appropriate ITR file as well as the tax regime.

- If a freelancer has no business income and only professional income, they can choose the preferred tax regime and can change it every year. This is possible when they declare their income as “Income from profession” in the ITR 3 or ITR 4 form. For example, if you selected the old tax regime for the FY 23-24, you can select the new tax regime for FY 24-25.

- Suppose a freelancer has a business income, i.e., income reported under “Profits and Gains from Business or Profession,” the rule changes. You can only opt for the new regime once. If you wish to switch to the old regime in the later years, you cannot opt back in unless you stop having business income altogether. Summing up, if you are a freelancer who also qualifies as a “business” (e.g., using ITR-3 for business income), then switching is limited.

- If you use presumptive taxation, which is for income less than ₹50 lakh, you can switch regimes without any hassle.

It’s always best to carefully review these details so that you don’t get caught up in any sort of mishaps or negligence.

What about Deductions?

Being a freelancer generally allows you to work from the comfort of your choice without any sort of hassle or sense of pressure. However, in the case of the bills that keep piling up, there isn’t much choice. A reasonable amount of your earnings goes into paying bills for various miscellaneous stuff that helps you to do your work efficiently. Fortunately, freelancers can reduce their taxable income by claiming expenses, similar to what businesses do.

Here are some examples of expenses that you could claim while filing.

- Laptop, printer, phone

- Internet bills

- Rent (if you work from home)

- Office furniture

- Travel (for shoots, meetings, etc.)

- Software subscriptions (Adobe, Canva, Notion, Zoom, etc.)

Placement Oriented PWC Business Accounting Course

PWC Certified Business Accounting Course by Entri App: Master in-demand skills, ace interviews, and secure top-tier jobs.

Join Now!Advance Tax & Deadlines for Freelancers

Freelancers with estimated tax liability exceeding ₹10,000 (and limited TDS coverage) must pay advance tax in installments to avoid interest penalties. This applies even under presumptive taxation like Section 44ADA. Use the ITNS 280 challan for payments via the e-filing portal or banks.

Advance Tax Schedule for AY 2026-27 (FY 2025-26)

Pay based on your projected annual tax after deductions. The table shows due dates and cumulative percentages of total liability.

| Installment | Due Date | Cumulative % |

|---|---|---|

| 1st | June 15 | 15% |

| 2nd | September 15 | 45% |

| 3rd | December 15 | 75% |

| 4th | March 15 | 100% |

Example: ₹50,000 total tax → 1st: ₹7,500 (by June 15); 2nd: ₹22,500 total (by Sep 15), and so on.

ITR Filing Deadlines

File your Income Tax Return (ITR) online via the e-filing portal. Deadlines depend on audit status.

- Non-audit cases (e.g., ITR-4 for professionals): July 31, 2026.

- Audit cases (e.g., ITR-3 with books): August 31, 2026.

- Belated returns: December 31, 2026, with a late fee of ₹5,000 (₹1,000 if income ≤ ₹5 Lakh).

Key Waivers and Penalties

- Exemptions: First-time filers with liability < ₹10,000 skip advance tax.

- Interest for delays:

- Section 234B: 1% per month on unpaid advance tax.

- Section 234C: 1% per month on installment shortfalls.

- Pro Tip: Estimate quarterly using the tax calculator; pay online for instant credit. Seniors (60+) have relaxed rules.

GST for Freelancers: When and How to Comply

Freelancers providing services (e.g., coding, writing, design) must check GST registration based on annual turnover. Exports like Upwork gigs are zero-rated—charge 0% GST but claim refunds. Register at gst.gov.in if required; it’s mandatory for most services at 18% GST rate.

When to Register

- Pan-India turnover ≥ ₹20 Lakh: Mandatory registration.

- Special states (e.g., Northeast) ≥ ₹10 Lakh: Mandatory.

- Exports/zero-rated supplies: Register to file LUT (Letter of Undertaking) for zero GST and input tax credit (ITC) refunds.

- Voluntary: Even below limits, to claim ITC on expenses like software/tools.

Turnover-Based Requirements

| Annual Turnover | GST Requirement | Filing Frequency |

|---|---|---|

| < ₹20 Lakh | Optional (nil returns if registered) | None or annual |

| ≥ ₹20 Lakh | Mandatory registration | Monthly/Quarterly GSTR-1 & 3B |

| ≥ ₹5 Crore (B2B supplies >5%) | E-invoicing mandatory | Same as above |

Notes:

- Turnover includes all taxable supplies (exclude pure exports).

- Quarterly filing for small taxpayers (turnover < ₹5 Crore): GSTR-1 by 13th, GSTR-3B by 22nd/24th.

Simple Registration Steps

- Visit gst.gov.in → New Registration → Verify PAN/Aadhaar.

- Upload docs (bank details, photo, address proof).

- For exports: File LUT annually (free bond) to avoid paying GST upfront.

- Claim ITC on business expenses (laptop, internet, software).

- File returns online; use GSTR-1 for invoices, GSTR-3B for summary payments.

Example: ₹25 Lakh Upwork income (exports) → Register, file LUT, zero GST output, claim ITC refunds.

Final Thoughts

ITR filing for freelancers may seem like an uncoquered mountain, but once you get the hang of it, you will be able to run through the procedure as easily as making a chai. However, if not made properly, even a simple chai can turn out to be a disaster. It is pretty common for one to wonder whether all of this hassle is worth it or not. The benefits of filing ITR are many, including claiming TDS/TCS refunds and visa processing, as the ITR file actually serves as proof of income.

The bottom line is that this is the ultimate proof of being a tax-paying citizen of India, with the added benefit of getting back extra taxes that you had to pay. By following the mentioned steps and common mistakes to avoid, you can make your ITR filing a seamless process. So, start the process now, and forget about penalties!

|

Courses Offered |

|

|

AI Powered Business Accounting and Finance Certification Programme |

SAP FICO Course |

Placement Oriented PWC Business Accounting Course

PWC Certified Business Accounting Course by Entri App: Master in-demand skills, ace interviews, and secure top-tier jobs.

Join Now!Frequently Asked Questions

Do freelancers in India need to pay income tax?

Yes. Freelancers are considered self-employed individuals under the Income Tax Act and must pay tax on income earned from freelance work, whether from Indian or foreign clients.

What is the minimum income limit for freelancers to file ITR?

You must file ITR if your total income exceeds:

-

₹2.5 lakh (Old Regime)

-

₹3 lakh (New Regime)

Even if your income is not consistent month-to-month.

Which ITR form should freelancers use?

-

ITR-3: For freelancers maintaining books of accounts.

-

ITR-4: For freelancers using Presumptive Taxation under Section 44ADA (income ≤ ₹50 lakh).

What's the turnover limit for Section 44ADA in 2026?

Limit is now ₹75 Lakh if ≥95% receipts are digital (UPI/bank)—check your receipts! Otherwise, ₹50 Lakh for any mode. Declare 50% as profit, no audits needed.

What types of income are taxable for freelancers?

-

Payments from Indian or international clients

-

Gigs or project income via platforms (Upwork, Fiverr, Behance, etc.)

-

Payments received via UPI, NEFT, IMPS

-

Any income shown in bank statements, even without a formal invoice

Can freelancers claim expenses as deductions?

Yes. Freelancers can deduct legitimate business-related expenses such as:

-

Internet, rent, and electricity bills

-

Laptop/software costs

-

Travel and marketing expenses

-

Subscription services (e.g., Adobe, Zoom)

-

Depreciation of business assets

Is TDS applicable to freelancers?

Yes. Clients may deduct TDS @10% under Section 194J before paying you. You can claim credit for this when filing ITR.

What is Form 26AS and AIS? Why are they important?

-

Form 26AS: Shows TDS deducted, advance tax paid, and other details.

-

AIS (Annual Information Statement): Provides a detailed record of all financial transactions (income, investments, etc.).

You must match your declared income with these documents.

Do freelancers need to pay advance tax?

Yes. If your tax liability exceeds ₹10,000 in a financial year, you’re required to pay advance tax in four installments (June, Sept, Dec, March).

Can freelancers switch between the old and new tax regimes every year?

Only if you don’t declare business income (i.e., use ITR-4 for presumptive or ITR-3 for profession only). If you declare business income, switching is allowed only once—after that, reverting is restricted.

{kind=link}