Table of Contents

Depending on whether they hold for less than or more than 12 months, mutual fund investors in India pay 20% or 12.5% tax on capital gains.

This may sound simple, but the actual tax liability shifts based on holding period, fund type, dividend income and also on whether you invested before or after April 1.

Budget 2026 kept core tax rates unchanged for Financial Year 2026-27. But at the same time it introduced a significant tweak that leveraged investors cannot afford to miss.

Key Takeaways:

- Equity mutual funds attract 20% Short-Term Capital Gains (STCG) tax for holdings up to 12 months. Also 12.5% Long-Term Capital Gains (LTCG) tax beyond 12 months, with the first ₹1.25 lakh in annual LTCG remaining tax-free.

- Debt funds purchased after April 1, 2023 are taxed entirely at your income slab rate – there is no LTCG benefit or indexation, regardless of how long you hold them.

- Dividend income from mutual funds is added to your total income and taxed at your applicable slab rate. From FY 2026-27, you can no longer deduct interest paid on borrowed funds used to earn this income.

- Hybrid funds follow equity taxation rules only if at least 65% of the portfolio is in domestic equities. Below that threshold, debt taxation applies.

- ELSS funds continue to qualify for a deduction of up to ₹1.5 lakh under Section 80C – but only under the old tax regime.

- Dividends are taxed at your income slab rate.

- A 4% health and education cess applies to all mutual fund tax liabilities.

- Budget 2026 made no changes to mutual fund tax rates; these are current.

Quick Reference: Mutual Fund Tax Rates at a Glance

| Fund Type | Holding Period | Tax Treatment |

| Equity Funds (≥65% equity) | ≤12 months | 20% STCG |

| Equity Funds | >12 months | 12.5% LTCG (above ₹1.25 lakh exempt) |

| Debt Funds (bought ≥ Apr 1, 2023) | Any period | Slab rate |

| Debt Funds (bought < Apr 1, 2023) | >24 months | 12.5% LTCG (no indexation) |

| Hybrid >65% equity | ≤12 months | 20% STCG |

| Hybrid >65% equity | >12 months | 12.5% LTCG |

| Hybrid ≤65% equity | >24 months | 12.5% LTCG |

| Gold ETFs (listed) | >12 months | 12.5% LTCG |

| Gold Mutual Funds / FoFs | >24 months | 12.5% LTCG |

| ELSS | Post 3-year lock-in | 12.5% LTCG (above ₹1.25 lakh) |

| Dividends | Any | Slab rate |

Mutual Funds and Indian Tax Law: The Basics

1: What is a stock?

-

Mutual funds in India are subject to capital gains tax and, in some cases, dividend tax.

-

Tax rules differ based on the type of fund: equity, debt, hybrid, or others (gold, international, and fund-of-funds).

-

The holding period, how long the units are held, determines whether the gains are short-term or long-term.

-

As of April 1, 2025, the Indian government has revised several definitions and taxation brackets for various fund categories.

Equity Mutual Funds: Taxation Rules

Definition

-

Equity mutual funds are schemes that invest at least 65% of their corpus in equity shares of domestic companies.

Tax Treatment

| Period Held | Type of Gain | Tax Rate | Exemption/Threshold | Notes |

|---|---|---|---|---|

| 12 months or less | Short-Term Capital Gain (STCG) | 15% | None | Surcharge and cess extra |

| More than 12 months | Long-Term Capital Gain (LTCG) | 12.5% on gains above ₹1.25 lakh | First ₹1.25 lakh tax-free | Indexation benefit unavailable |

Example

If total LTCG in a financial year equals ₹1.45 lakh, only ₹20,000 is taxable at 12.5%; ₹1.25 lakh remains exempt.

Dividend Tax

All mutual fund dividends are taxed in the hands of investors as per the applicable income tax slab.

Start investing like a pro. Enroll in our Stock Market course!

Non-Equity Mutual Funds: Taxation Rules

Definition

-

Debt mutual funds are those where more than 65% of the portfolio is invested in debt instruments, such as government securities or corporate bonds.

Latest Update (Effective April 1, 2025)

| Period Held | Type of Gain | Tax Rate | Notes |

|---|---|---|---|

| Up to 2 years | Short-Term Capital Gain (STCG) | As per the investor’s income tax slab | No indexation benefit |

| More than 2 years | Long-Term Capital Gain (LTCG) | 12.5% | No indexation benefit; earlier LTCG was taxed at 20% with indexation pre-2023 |

Older Investments

-

If the investment is made before April 1, 2023, LTCG is taxed at 20% with indexation if held for over 3 years.

-

Investments between April 1, 2023, and March 31, 2025, are taxed as per slab rate, regardless of holding period.

Dividend Tax

-

Dividends are taxed as per the individual’s income tax slab.

| Gain Financial Literacy in your Mother Tongue | |

| Stock Market Course in Malayalam | Mutual Funds Course in Malayalam |

| Stock Market Course in Tamil | Mutual Funds Course in Tamil |

| Stock Market Course | Mutual Funds Course |

Hybrid, International, Gold, and Fund of Funds

| Fund Type | STCG (Holding Period) | STCG Tax Rate | LTCG (Holding Period) | LTCG Tax Rate | Threshold/Notes |

|---|---|---|---|---|---|

| Equity-Oriented Hybrid | ≤12 months | 15% | >12 months | 12.5% (₹1.25L exempt) | ≥65% in equity |

| Debt-Oriented Hybrid | ≤2 years | As per the slab | >2 years | 12.5% | <65% in equity |

| Gold, International, FoF | ≤2 years | As per the slab | >2 years | 12.5% | No indexation benefit post-2025 |

-

International and gold funds, as well as fund-of-funds, follow the new debt fund taxation structure from April 1, 2025.

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

Know moreKey Taxation Concepts Explained

What Are Capital Gains?

-

Capital Gains are profits realized from selling mutual fund units. Tax treatment depends on type and holding period.

Short-Term vs. Long-Term: How Is “Period Held” Calculated?

-

Equity funds: Less than or equal to 12 months: STCG; More than 12 months: LTCG.

-

Debt funds, international, gold, FoFs: Less than or equal to 2 years: STCG; More than two years: LTCG.

Indexation

-

Indexation allows investors to adjust the purchase price by inflation, reducing taxable gains.

-

Indexation benefit is NO LONGER AVAILABLE for new investments in debt funds, international, gold, and FoFs post April 1, 2026.

How To Calculate Tax on Mutual Fund Gains

For Equity Mutual Funds:

-

Calculate net gain = Redemption value – (Purchase value + charges)

-

Identify holding period.

-

Apply STCG or LTCG rule:

-

STCG: Tax at 15%

-

LTCG: Up to ₹1.25 lakh tax-free; 12.5% on excess.

-

Debt Mutual Funds:

-

Determine holding period.

-

If ≤2 years: Add gain to total income, taxed by slab.

-

If >2 years (for investments post-April 1, 2026): 12.5% tax, no indexation benefit.

SIPs (Systematic Investment Plans):

-

Each SIP installment is treated as a separate investment for determining the holding period and tax applicability.

Dividend Taxation

-

Post-April 2020, dividends are added to investors’ income and taxed as per their income tax slab (no Dividend Distribution Tax at the fund level).

-

TDS (Tax Deducted at Source) at 10% applies if the dividend payout exceeds ₹5,000 in a financial year for resident individuals.

Securities Transaction Tax (STT)

STT is applicable to transactions of equity mutual funds on the stock exchange.

-

Tax Rate: 0.1% on both buying and selling equity mutual funds through an exchange.

| Type of Fund | Tax on Transactions | STT Rate |

|---|---|---|

| Equity Mutual Funds | On buying/selling units | 0.1% |

| Debt Mutual Funds | Not applicable | N/A |

TDS Rules for NRIs

-

For NRIs, TDS is deducted at 20% for equity-oriented and 30% for non-equity schemes, including cess and surcharge, on capital gains and dividend payouts.

-

A rebate or refund can be claimed at the time of filing returns if the actual tax liability is lower.

Tax Filing and Compliance Tips

How to Report Mutual Fund Gains in ITR

-

All capital gains, short or long term, must be disclosed in the appropriate schedules of your ITR (ITR-2/3 for individuals with capital gains).

-

Fund houses usually provide capital gain statements that help in reporting the correct figures.

-

One must also report dividend income separately under the head ‘Income from Other Sources’.

Important Considerations

-

For investments held jointly, tax liability belongs to the first holder as per PAN details.

-

Losses from mutual funds, short-term or long-term, can be set off against gains of the same nature and carried forward up to 8 years.

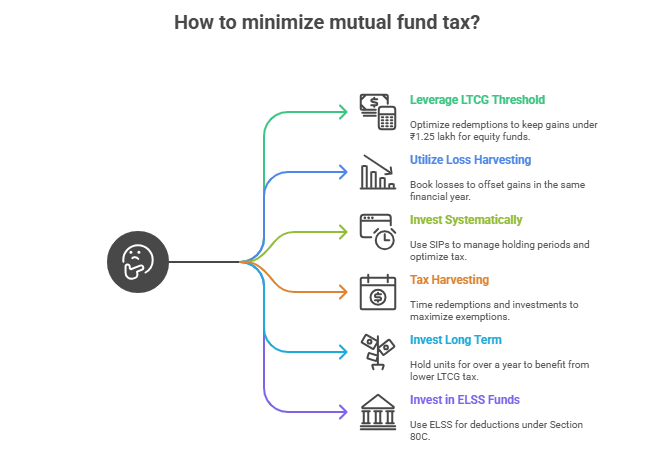

Expert Tips on Minimizing Mutual Fund Tax

-

Leverage LTCG Threshold: Optimize redemptions to keep annual long-term capital gains under ₹1.25 lakh for equity funds.

-

Utilize Loss Harvesting: Book losses where suitable to offset gains in the same financial year.

-

Invest Systematically: SIPs provide flexibility to manage holding periods, optimizing between STCG and LTCG.

-

Tax Harvesting: Time redemptions and new investments to maximize tax exemption limits and minimize slab-based liability.

- Invest for the Long Term: Holding equity mutual fund units for more than 1 year allows you to benefit from LTCG tax at 10% (above ₹1 lakh), which is more favorable than STCG tax at 15%.

- Invest in Tax-Saving ELSS Funds: Equity Linked Savings Schemes (ELSS) are eligible for deductions under Section 80C of the Income Tax Act, offering a tax-saving option up to ₹1.5 lakh annually.

Equity Mutual Funds: Tax Rules for FY 2026-27

Equity mutual funds are those that invest at least 65% of their corpus in domestic equities. These funds enjoy relatively favourable tax treatment when compared to other debt-oriented options.

Short-Term Capital Gains (STCG):

If you sell your equity fund units within 12 months of purchase, your gains are treated as short-term. It will be taxed at a flat rate of 20%, regardless of your income bracket.

Long-Term Capital Gains (LTCG):

Hold for more than 12 months, and only gains exceeding ₹1.25 lakh in a financial year are taxable at 12.5%. Gains within that ₹1.25 lakh annual threshold remain completely tax-free. This exemption is cumulative across all equity-related investments, not per fund.

| Holding Period | Gain Classification | Tax Rate | Exemption |

| Up to 12 months | Short-Term Capital Gain | 20% | None |

| More than 12 months | Long-Term Capital Gain | 12.5% | ₹1.25 lakh per year |

A quick example:

You invested ₹2 lakh in an equity mutual fund and redeemed after 14 months for ₹3.25 lakh. Your total gain is ₹1.25 lakh. Since this falls within the annual LTCG exemption, your tax liability is zero. If your gain were ₹1.75 lakh instead, only ₹50,000 would be taxable — translating to ₹6,250 in tax at 12.5%.

SIP Taxation: Each Instalment is Treated Separately

A Systematic Investment Plan (SIP) does not work as a lump-sum purchase for tax purposes. Each SIP instalment is treated as a separate investment with its own purchase date. The FIFO (First In, First Out) method is applied during redemption.

This means if you start a monthly SIP in January 2024 and redeem all units in February 2025:

- The January 2024 instalment has been held for 13 months. It qualifies as LTCG (if equity).

- The February 2025 instalment has been held for only 1 month. It qualifies as STCG.

Investors who redeem SIP portfolios without factoring in per-instalment holding periods often find themselves with unexpected STCG liability on recent installments.

Dividend Taxation and the FY 2026-27 Change

Dividends declared by mutual funds are credited to your bank account and taxed as income from other sources at your slab rate and not at a flat capital gains rate.

TDS is deducted at 10% if your total dividend income from a fund house exceeds ₹5,000 in a financial year (for resident investors). You can claim credit for this TDS when filing your ITR.

The FY 2026-27 change:

Starting April 1, 2026, investors who borrow money and use it to invest in mutual funds can no longer deduct the interest cost against dividend income.

Previously, such a deduction was permitted. This primarily impacts leveraged investors and high-net-worth individuals who used borrowed capital to earn dividend income.

Tax-Saving Strategies that Actually Work

You do not have to resign yourself to paying maximum taxes on mutual fund gains. A few smart moves can meaningfully reduce your liability.

Hold equity funds long-term

Staying invested beyond 12 months automatically shifts you from 20% STCG to 12.5% LTCG. Combined with the ₹1.25 lakh annual exemption, patient investors can often bring their effective tax rate close to zero on moderate gains.

Tax-loss harvesting

If some funds in your portfolio are in the red, consider redeeming them before the financial year ends. The booked losses can offset gains from other funds. Short-term losses can offset both STCG and LTCG; long-term losses can only offset LTCG. Carry-forward is allowed for up to 8 years.

Stagger redemptions to stay within the LTCG exemption

If your equity fund gains are approaching ₹1.25 lakh, consider redeeming part of the portfolio this financial year and the rest in the next. Each financial year gets its own ₹1.25 lakh exemption.

Use ELSS for Section 80C benefits

Equity Linked Savings Schemes (ELSS) offer a deduction of up to ₹1.5 lakh under Section 80C if you are in the old tax regime. They have a mandatory 3-year lock-in period, but they are also the most tax-efficient equity fund category from an entry standpoint.

File correctly

Capital gains from mutual funds must be reported in ITR-2 (for individuals without business income) or ITR-3. Use your Consolidated Account Statement (CAS) or individual fund statements to calculate gains accurately. For joint holdings, the first holder is responsible for paying tax on all gains.

What Budget 2026 Changed (And What Stayed the Same)

Budget 2026 was largely a status-quo year for mutual fund investors. Here is a quick summary of what changed and what did not:

Unchanged:

- Equity STCG rate: 20%

- Equity LTCG rate: 12.5%

- Annual LTCG exemption: ₹1.25 lakh

- Debt fund slab-rate taxation (for post-April 2023 purchases)

- STT on equity mutual fund transactions: 0.1%

New from FY 2026-27:

- Interest paid on borrowed funds used to invest in mutual funds can no longer be deducted against dividend or mutual fund income. This rule came into effect on April 1, 2026.

The STT hike in Budget 2026 applied only to derivative instruments — equity mutual funds were not affected.

Conclusion

Mutual fund taxation in 2026 follows a cleaner framework than it once did, but the details still matter. The broad picture: equity funds reward long-term investors with a 12.5% LTCG rate and a ₹1.25 lakh annual exemption.

Debt funds bought after April 2023 offer no such relief. Everything is taxed at your slab rate. And the choice between dividend and growth options can make a meaningful difference to your actual returns, especially in higher tax brackets.

The single most valuable habit you can build is tracking your holding period for every investment, not just roughly, but precisely. A few weeks’ difference can determine whether a gain is short-term or long-term, and that can mean thousands of rupees in tax saved or unnecessarily paid.

When in doubt, run the numbers before you redeem. A little planning goes a long way.

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

Know moreFrequently Asked Questions

Is SIP investment tax-free?

No, SIP returns from mutual funds are subject to capital gains tax as per the respective holding period and fund type. Each SIP installment is a separate investment.

How are hybrid funds taxed?

Depends on the equity component:

-

≥65% in equity: Treated as equity fund

-

<65% in equity: Treated as a debt fund for taxation.

Do mutual fund gains attract TDS?

Only if the payee is an NRI or if the dividend income exceeds ₹5,000 for residents. No TDS on capital gains for resident individuals.

What is the tax rate on equity mutual fund gains?

Short-term capital gains (STCG) on equity mutual funds (units held for 12 months or less) are taxed at 20%. Long-term capital gains (LTCG) on equity mutual funds (held for more than 12 months) are taxed at 12.5% on gains above ₹1.25 lakh per year.

Do I pay tax on unrealised gains?

No. Tax on mutual fund capital gains is triggered only when you redeem your units. Unrealised gains within a held investment attract no tax.

Are Gold ETFs taxed the same as equity funds?

No. Gold ETFs are not equity-oriented. They qualify for 12.5% LTCG after 12 months, but short-term gains are taxed at your income slab rate — not at the flat 20% STCG rate that applies to equity funds.

{kind=link}