Table of Contents

Yes, investing in mutual funds – specifically ELSS (Equity Linked Savings Scheme) – can help you save up to ₹46,800 in taxes every year under Section 80C of the Income Tax Act.

Unlike traditional instruments that force you to choose between saving taxes and growing wealth, ELSS does both simultaneously. With historically average returns of 12% to 16% and the shortest lock-in period among all Section 80C options, ELSS has become one of India’s most efficient tax-saving investment tools.

But before you rush to invest, there’s a critical heads up for you – ELSS tax benefits are available only under the old tax regime. If you’ve switched to the new tax regime, the Section 80C deduction doesn’t apply. This guide covers everything you need to make a well-informed decision in 2026.

Key Takeaways

- ELSS is the only mutual fund eligible for Section 80C, up to ₹1.5 lakh/year.

- Maximum annual tax saving is ₹46,800 for the 30% bracket (including 4% cess).

- Lock-in period is 3 years, the shortest among 80C options.

- After lock-in, LTCG above ₹1.25 lakh is taxed at 12.5%; gains below that are tax-free.

- ELSS tax benefits apply only under the old tax regime.

- Each SIP installment has its own 3-year lock-in from its investment date.

- Historical ELSS returns are about 12–16% p.a., higher than PPF (~7–8%) and tax-saving FDs (~6–7%).

- SIP investments start from ₹500/month.

Click here to learn more about mutual funds and ELSS from expert investors! Join Entri now!

What are Mutual Funds?

1: What is a stock?

Mutual funds are professionally managed investment vehicles that pool money from multiple investors and deploy it across stocks, bonds, or a mix of both. This is done based on the fund’s objective. A professional fund manager makes investment decisions on your behalf.

The key advantage? You get access to diversified, market-linked investments without needing deep expertise or large capital. SIPs (Systematic Investment Plans) make it even more accessible as you can start with as little as ₹500 per month. Among all mutual fund types, ELSS is the one that comes with built-in tax-saving potential.

You might find it difficult to believe, but it is true! Mutual funds can not only help us build wealth but also help us save taxes. Equity Linked Savings Scheme (ELSS) is one of the schemes that stands out among other tax-saving mutual funds in India. As we discussed above, this scheme comes with dual benefits. They are:

- Tax deductions under Section 80C

- Potential market-linked growth

ELSS has soon become a favoured choice among investors in India, especially after India’s new tax regime. In this blog, we will dive deep into mutual fund tax savings, what ELSS is, how it works, its advantages, and comparisons with other instruments. We will also discuss practical steps for starting your investment journey.

Can Investing in Mutual Funds Help You Save Taxes in India? (Complete Guide)

This is a very important question that comes to the mind of every beginner investor. Let us tackle this question from the very base level. Let us learn what mutual funds are first.

What is ELSS (Equity Linked Savings Scheme)?

Equity Linked Savings Scheme (ELSS) is a category of equity mutual fund. It is specially designed for achieving the purpose of tax savings. Let us learn more about the ELSS instrument.

| Feature | Details |

| Investment Focus | Invests at least 80% in equities

Diversified across sectors and market caps |

| Lock-in Period | Fixed 3-year lock-in

Shortest among Section 80C options |

| Tax Deduction | Up to ₹1.5 lakh deductible under Section 80C

Max tax savings: ₹46,800 (30% slab) |

| Investment Modes | Lump sum or SIP options available

Flexible for all types of investors |

How Does ELSS Help You Save Tax?

Now you might be wondering, how does ELSS help us save tax? We will explain it in the simplest way possible. ELSS investors can claim deductions of up to ₹1.5 lakh per financial year under Section 80C of the Income Tax Act. This reduces taxable income and hence lowers tax liability. For example, up to ₹46,800 saved at a 30% tax rate, including cess. Then there is the fact that gains up to ₹1 lakh are completely tax-free. After the 3-year lock-in, long-term capital gains (LTCG) beyond ₹1 lakh in a year are taxed at 10% (no indexation benefit).

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

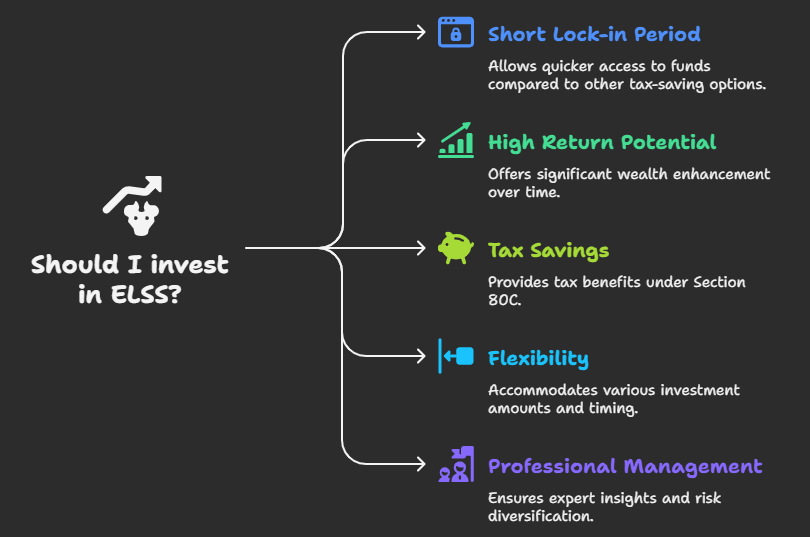

Know moreBenefits of Investing in ELSS

Let us take a look at some benefits of investing in ELSS.

| Benefit | Details |

| Shortest Lock‑In | Only 3-year lock-in period

More liquid than PPF (15 years) and FDs/NSC (5 years) |

| High Return Potential | 7, 10, and 15-year average returns ~15%

Some reports show ~16.26% average returns |

| Dual Benefit | Saves tax under Section 80C

Offers market-linked growth for long-term wealth creation |

| Flexibility | Choose between SIP or lump sum

Open-ended; invest any time- SIPs support cost averaging |

| Professional Management and Diversification | Run by experienced fund managers

Diversified across sectors and market caps- Lowers concentration risk |

| Gain Financial Literacy in your Mother Tongue | |

| Stock Market Course in Malayalam | Mutual Funds Course in Malayalam |

| Stock Market Course in Tamil | Mutual Funds Course in Tamil |

| Stock Market Course | Mutual Funds Course |

Things to Keep in Mind Before Investing

Market risk is real:

ELSS invests heavily in equities. Short-term NAV fluctuations are normal. Investors need a moderate-to-high risk appetite and should ideally stay invested beyond the 3-year lock-in for better outcomes.

SIP lock-in works differently:

Each SIP instalment starts its own individual 3-year clock. If you invest via SIP from January 2026, your January 2026 instalment unlocks in January 2029, February 2026 instalment in February 2029, and so on.

Expense ratio matters:

Even a 0.5% difference in expense ratio can meaningfully impact your net returns over 10+ years. Always compare this before choosing a fund.

Don’t invest only in March:

Many people panic-invest in ELSS at the end of the year-end. Starting a SIP in April gives your money a full 12 months of compounding before you even claim the deduction.

Even with all these benefits, there are some things that you should keep in mind while investing in ELSS. Some of them are discussed below.

| Consideration | Details |

| Market Risk | Equity-heavy; returns may fluctuate

Suitable for investors with risk tolerance |

| Due‑Diligence | Review past fund performance

Check fund manager’s track record Evaluate expense ratio, Sharpe ratio, alpha & beta |

| Lock‑In Clarity | Each SIP instalment is locked in for 3 years

Plan withdrawals accordingly |

| Tax Regime Shift | New tax regime excludes Section 80C benefits

ELSS less attractive if you’ve opted for the new regime |

| LTCG Implication | Gains above ₹1 lakh/year taxed at 10%

Consider tax while planning redemptions |

ELSS vs Other Tax-Saving Instruments

A table that compares ELSS vs other traditional tax-saving instruments is given below so that you can understand the concepts discussed in this blog better.

| Investment Option | Lock‑in Period | Risk Level | Returns | Tax Deduction (80C) | Taxation on Gains |

| ELSS | 3 years | High (Equities) | ~12–16% historically | Up to ₹1.5 lakh | LTCG > ₹1 lakh taxed at 10% |

| Public Provident Fund (PPF) | 15 years | Low | ~7–8% (EEE) | Up to ₹1.5 lakh | Fully tax-exempt |

| Fixed Deposits (5‑yr Tax FD) | 5 years | Low | ~6–7% | Up to ₹1.5 lakh | Interest fully taxable |

| National Savings Certificate (NSC) | 5 years | Low | ~7–8% | Up to ₹1.5 lakh | Interest is taxable (and reinvested) |

| National Pension System (NPS) | Until retirement | Moderate–High | Market-linked (~7–8%) | Up to ₹1.5 lakh | Tax on 60% of corpus at withdrawal |

How to Start Investing in ELSS?

Now that we understand both benefits and risks involving ELSS, you must be wondering how you can start investing in ELSS. We have an answer for this question too.

Learn how mutual fund tax savings through ELSS can help you reduce taxable income under Section 80C while building long-term wealth.

| Step | Details |

| Determine Your Investment Strategy | Choose between lump sum or SIP

SIPs start as low as ₹500/month Promote discipline and cost averaging |

| Research Fund Options | Compare past fund performance

Evaluate fund manager’s track record Check risk measures and expense ratio |

| KYC First | Complete Know-Your-Customer (KYC) process

Mandatory for all mutual fund investments |

| Choose a Platform | Invest through AMC websites, aggregators, or mobile apps

Pick between growth and dividend options |

| Monitor & Hold | Stay invested even after lock-in for better returns

Regularly monitor fund performance and rebalance if needed |

Smart Tax Harvesting with ELSS

Tax harvesting is a legal strategy to optimize your tax liability every year. Here’s how it works with ELSS:

After the 3-year lock-in, identify units with gains below ₹1.25 lakh. Redeem them to “book” tax-free gains, then reinvest the amount. This resets your cost base without triggering tax, effectively reducing your future taxable capital gains.

Best time to do this: Before March 31 each year to use the full ₹1.25 lakh annual exemption.

Common Mistakes ELSS Investors Make

Investing only at year-end:

Starting your SIP in April instead of March gives you 12 additional months of compounding per year. Over a decade, this difference is significant.

Redeeming right after 3 years:

Many investors treat ELSS as a 3-year FD. That’s a costly mistake. The fund’s equity nature means long-term holding (5–7+ years) is where real wealth is built.

Ignoring the tax regime:

Investing in ELSS under the new tax regime and expecting a Section 80C benefit is a common misconception. Verify your tax regime before investing.

Not tracking SIP lock-ins:

Trying to withdraw an entire SIP portfolio together often fails because some installments may still be within their 3-year period. Plan redemptions installment-wise.

Click here to learn more about the Entri Elevate stock trading course! Join now!

Conclusion

ELSS remains one of India’s most well-rounded tax-saving investment options, if you’re on the old tax regime. It delivers what most traditional instruments can’t: tax savings on entry, market-linked growth during the holding period, and a relatively short lock-in of just 3 years.

With LTCG gains up to ₹1.25 lakh exempt from tax annually and historical returns consistently outperforming fixed-income alternatives, the case for ELSS is compelling for long-term equity investors. However, the shift toward India’s new tax regime has made the upfront tax deduction less accessible for a growing number of taxpayers.

The right approach: evaluate your tax regime first, understand your risk appetite, start early in the financial year, invest via SIP, and stay invested well beyond the lock-in period. Tax saving should be a smart by-product of disciplined investing and not a last-minute rush.

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

Know moreFrequently Asked Questions

Can mutual funds help you save taxes in India?

Yes, but specifically through ELSS (Equity Linked Savings Scheme). ELSS is the only mutual fund category eligible for a deduction under Section 80C of the Income Tax Act, allowing you to reduce your taxable income by up to ₹1.5 lakh per year. This benefit applies only under the old tax regime.

How much tax can I save by investing in ELSS?

If you’re in the 30% tax bracket and invest the full ₹1.5 lakh in ELSS, you can save up to ₹46,800 per year (including 4% health and education cess). The saving is ₹31,200 at the 20% bracket and ₹7,800 at the 5% bracket.

What is the lock-in period for ELSS?

ELSS has a mandatory lock-in of 3 years from the date of investment. This is the shortest lock-in period among all Section 80C instruments. For SIP investments, each installment has its own individual 3-year lock-in period.

Are ELSS returns taxable?

After the 3-year lock-in, returns from ELSS are treated as Long-Term Capital Gains (LTCG). Gains up to ₹1.25 lakh per financial year are completely tax-free. Gains above ₹1.25 lakh are taxed at 12.5% without the benefit of indexation.

Can I invest in ELSS under the new tax regime?

You can invest, but the Section 80C tax deduction does not apply under the new tax regime. So, while ELSS remains a valid equity investment, it won’t reduce your taxable income if you’ve opted for the new regime.

What is the minimum amount I can invest in ELSS?

You can start investing in ELSS with as little as ₹500 per month through a SIP. For a lump sum, the minimum varies by fund but is generally ₹500–₹1,000.

What happens if I miss a SIP instalment in ELSS?

Missing a SIP installment does not affect your existing investments. Each completed installment continues with its own 3-year lock-in. You simply won’t receive the 80C benefit for the missed amount in that financial year.

{kind=link}