Table of Contents

Gold remains a trusted asset globally. People still ask: is-gold-a-good-investment today? Its demand rises during uncertain financial times. Many investors use gold for safety. It protects wealth against currency decline. History shows gold survives every crisis. It carries emotional value in India. People also view it as backup savings. Gold continues to symbolise security.

Modern investors also look at returns. They want stability with low risk. Gold offers safety, not quick profit. It balances a long-term portfolio. Investments need diversification for security. Gold plays that stable role well.

Even small allocation gives confidence. It supports growth by reducing risk.

Learn Stock Marketing with a Share Trading Expert! Explore Here!

Why do people still choose gold?

-

It protects wealth during inflation.

-

It stays valuable over decades.

-

Easy to sell anytime.

-

Trusted by generations worldwide.

-

Acts as safety during market crashes.

1. Introduction

Gold is seen as a timeless asset. People across generations trust its value. It maintains worth even during tough times. Investors treat it as safe protection. Gold behaves differently during market stress. That is why many prefer gold. Emotions also influence gold buying habits. In India, gold equals family security. It is both tradition and safety.

Global investors also rely on gold. They use gold during uncertain periods. It protects savings from global shocks. Wars or recessions boost gold demand. Economic fear pushes people toward gold. It offers comfort when markets crash. That trust keeps demand always steady. Gold therefore remains widely relevant.

Before investing, evaluation is important. Every asset has pros and limits. Gold gives safety, not quick profit. It cannot replace growth investments. It supports overall financial planning well. For many, gold is backup wealth. But it should be balanced wisely. Right allocation gives better stability.

Why understanding gold matters today

-

Markets are uncertain globally now.

-

Inflation affects purchasing power directly.

-

Investors seek safe and stable assets.

-

Gold protects value during economic stress.

-

It improves long-term portfolio balance.

2. Historical Significance of Gold

1: What is a stock?

2.1 Gold as a Store of Value

Gold has held value for centuries. Kings and traders trusted gold universally. It was used before paper currency existed. People used gold for major transactions. It acted like natural money everywhere. Gold remained valuable across all regions. Its worth never depended on governments. That made gold truly timeless wealth.

Why gold stayed valuable

-

It is rare and limited.

-

It cannot be destroyed easily.

-

It holds universal acceptance.

-

It maintains value across eras.

2.2 Gold as Currency in History

Gold coins were official currency earlier. Empires kept reserves in gold. It built trust during trade deals. Merchants accepted gold without hesitation. The “gold standard” backed currencies globally. Nations stored gold for financial strength. Strong reserves signaled strong economy. Gold enabled global financial stability.

| Time Period | Role of Gold | Purpose |

|---|---|---|

| Ancient Era | Medium of exchange | Trade and wealth |

| Medieval Era | Royal treasure | Power and control |

| Colonial Era | Reserve asset | Global trade settlement |

| Early 1900s | Currency backing | Gold standard system |

| Modern Era | Financial hedge | Crisis protection |

2.3 Gold During Crises and Inflation

Gold protects wealth during inflationary periods. When currency weakens, gold strengthens. People buy gold during economic fear. It acts like financial insurance always. Stock crashes push money toward gold. That demand increases its long-term value. Hence gold behaves like crisis shield. It preserves purchasing power effectively.

Examples of gold stability

-

During recessions, gold stays strong.

-

During wars, demand increases fast.

-

During inflation, value rises steadily.

-

When markets fall, gold outperforms.

| Economic Situation | Currency Impact | Gold Impact |

|---|---|---|

| Inflation spike | Value declines | Gold rises |

| Market crash | Stocks drop | Gold gains |

| War or tension | Fear increases | Demand rises |

| Policy uncertainty | Trust falls | Gold strengthens |

2.4 Why History Still Matters Today

Old patterns repeat during stress. Gold reacts similarly in every crisis. Human trust keeps gold relevant always. That is why investors still choose gold. History supports gold’s strong reputation. It worked before, so trust remains.

Gold is popular for many solid reasons. It protects value during unstable situations. People trust it for financial security. It balances overall investment risk smartly. Gold protects money from inflation impact. When prices rise, gold usually rises too. It keeps purchasing power more stable. Currency loses value, gold holds value. Gold moves opposite to currency decline. Supply is limited, demand stays strong. People prefer hard assets during inflation. Value preserved without government control. Gold is extremely easy to liquidate. It sells quickly in most markets. You can convert gold into cash immediately. No long waiting period is required. Instant selling options everywhere. Buyers available in all regions. Quick emergency cash possible. No complex process involved. Gold reduces overall portfolio risk. It balances volatile assets like stocks. Gold performance differs from equities. It helps maintain portfolio stability. Provides safety cushion. Limits heavy portfolio loss. Works during stock crashes. Supports long-term confidence. Gold performs best in uncertain times. People choose gold during global fear. It is trusted during wars or recessions. Safety perception boosts demand further. During geopolitical tension. During banking failure fears. During market panic phases. During currency instability. Invest Smart, Learn Faster – Mutual Fund Course for Kerala Gold is useful but not perfect. It carries some important limitations. Understanding these helps wiser investing. Gold must be used with balance. Gold does not pay interest. Gold does not give dividends. It only grows through price rise. There is no cash flow. Income seekers gain nothing monthly. Growth depends only on appreciation. It cannot replace salary income. Passive income sources work better. Gold prices fluctuate frequently. Short-term charts show wide swings. Quick buying may feel risky. Timing mistakes reduce gains. Sudden global news updates. Rupee-dollar movement changes. Trader speculation spikes prices. Demand supply imbalance occurs. Physical gold needs safe storage. Jewel gold carries making charges. Selling deducts wastage cost also. Security costs reduce final return. Locker rent yearly. Insurance expenses possible. High making charges. Resale deduction applied. Gold depends on global events. Dollar strength affects gold price. US interest rates move gold. Global demand impacts valuation. US monetary policies. Global recession signals. Currency fluctuations globally. Central bank decisions. Gold can be purchased in many forms. Each method suits different investor needs. Some offer safety, some offer liquidity. Your choice depends on goals. Physical gold includes jewellery, coins, bars. It is the traditional buying method. People prefer it for cultural reasons. However, it carries extra expenses. Tangible real asset. Trusted for generations. Emotionally valued in India. Easy for gifting. Making charges apply. Storage risk exists. Resale deduction possible. Security costs added. Gold ETFs are easy market products. They track gold price digitally. No storage cost is required. They allow transparent trading anytime. Gold mutual funds invest in ETFs. They suit non-Demat investors easily. Both provide safer gold exposure. Returns follow gold movement closely. SGBs are issued by RBI. They give fixed interest annually. Value also grows if price rises. Storage cost is zero here. 2.5% yearly interest income. Zero making charges. Tax benefit on maturity. Very safe government instrument. Digital gold is app-based purchase. You can buy micro quantities easily. It suits small new investors well. Platform stores gold safely. Instant purchase online. No minimum limit required. Easy liquidity option available. Convenient for beginners. Platform charges sometimes apply. Not regulated like SGBs. Long holding risk exists. Conversion may need extra fee. Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

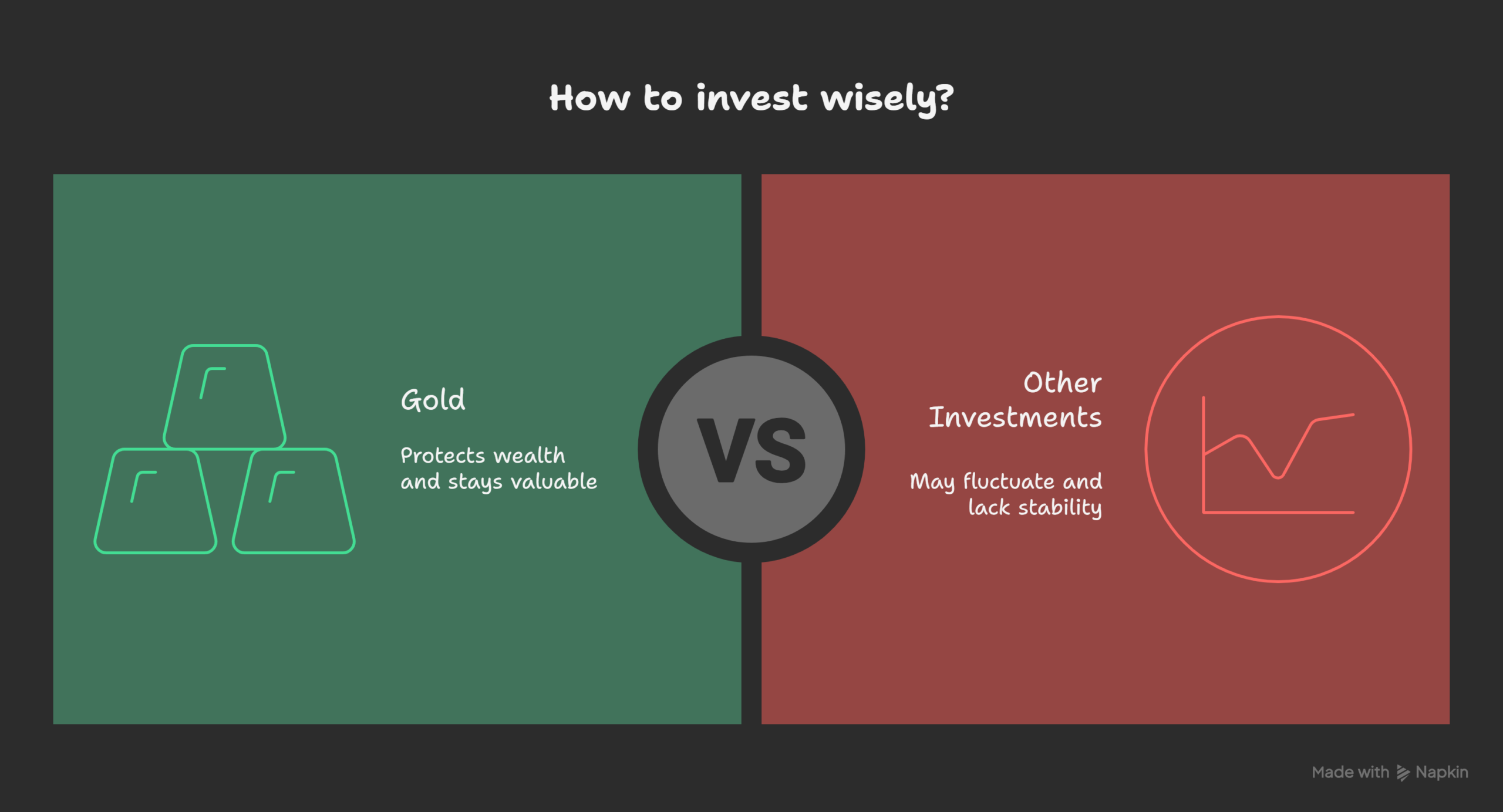

Gold works best during unstable conditions. It protects portfolios during market fear. Investors prefer gold when risk increases. It balances other assets efficiently. Gold outperforms most assets during inflation. Rising prices reduce currency strength. People shift toward safer assets. Gold preserves true purchasing power. Value stays relatively stable. Currency erosion gets offset. Price appreciation creates protection. Public confidence remains high. Gold reacts strongly to global uncertainty. Fear increases safe-haven demand quickly. People buy gold during crises worldwide. It becomes a trust-based shield. Wars or geopolitical conflicts. Financial market crashes. Recession or slowdown warnings. Global banking instability. Gold works best as partial allocation. Not entire wealth, but balanced share. It complements other asset classes. Acts like long-term protection layer. Keep moderate exposure only. Avoid full dependency on gold. Use gold for stability buffer. Let other assets drive growth. Invest Smart, Learn Faster – Mutual Fund Course for Kerala Gold is useful but not complete. It gives safety, not heavy growth. Other assets grow wealth faster. Each asset plays different roles. Stocks give higher long-term growth. Gold protects, stocks create wealth. Stocks move with economic performance. Gold moves with global fear. Real estate builds long-term assets. Gold is simpler and more liquid. Property offers rental income. Gold offers easier exit option. FDs give stable interest earnings. Gold does not provide interest. FDs are predictable income sources. Gold is inflation protection tool. Mutual funds create long-term growth. Gold secures capital during stress. Mutual funds suit wealth building. Gold is support, not core asset. It protects, but rarely multiplies. A smart portfolio blends both. Balance gives better financial health. Gold remains a reliable safety asset today. It protects wealth during unstable market periods. People trust gold across generations globally. Its value survives inflation and financial shocks. Gold stabilizes portfolios during economic fear. It works best as long-term protection. Not a growth tool, but a hedge. Gold maintains confidence when markets fall. It supports financial security steadily. Gold should not replace growth assets. It must stay a supporting investment. Balanced allocation gives better wealth outcomes. Even small holding improves portfolio strength. Right timing enhances inflation protection. Long-term patience improves gold benefits. Disciplined allocation ensures reliable stability. Gold works best with diversification. RELATED POSTS Trusted, concepts to help you grow with confidence. Enroll now and learn to start investing the right way.

Yes, gold is widely considered a safe-haven investment due to its ability to preserve wealth over time. It is not dependent on the performance of any single economy or stock market, making it reliable during financial crises. Investors turn to gold when currencies weaken or stock markets decline. Historically, gold has maintained its value even during wars, recessions, and periods of high inflation. While it does not generate income like dividends or interest, its stability and universal acceptance make it a trusted option for long-term wealth protection. Financial experts recommend allocating between 5% to 15% of your total investment portfolio to gold. This allocation is enough to provide stability without reducing the potential for higher returns from growth-oriented assets like stocks or mutual funds. Too much gold in a portfolio may limit income and growth opportunities because it does not provide regular returns. A moderate allocation helps hedge against inflation and market volatility. Individual allocation may vary depending on risk tolerance, financial goals, and current economic conditions. Gold does not provide regular income in the form of dividends or interest, unlike stocks or fixed deposits. Its returns are mainly based on price appreciation over time or, in the case of Sovereign Gold Bonds (SGBs), a fixed interest of 2.5% per annum. Physical gold, digital gold, and ETFs do not generate recurring income and rely solely on market price movement. Investors looking for regular cash flow need to complement gold with other income-generating assets. However, its value preservation and safe-haven characteristics make gold a critical component for long-term security. There are multiple ways to invest in gold depending on your preferences, risk appetite, and convenience. Physical gold includes jewellery, coins, and bars, which are tangible but involve storage costs and making charges. Gold ETFs and mutual funds allow digital exposure and are easier to trade without storage concerns. Sovereign Gold Bonds (SGBs) offer government-backed safety with additional annual interest and tax benefits on maturity. Digital gold platforms provide a convenient way to invest small amounts instantly, although some may charge fees for buying or converting gold. Choosing the right method depends on whether your focus is safety, liquidity, or long-term returns. Gold is considered a hedge against inflation because its value generally rises when the purchasing power of currency declines. During periods of high inflation, prices of goods and services increase, but gold prices typically move upward, helping investors preserve real wealth. This happens because gold is a finite resource with consistent demand globally, unlike fiat currencies that can be printed in unlimited supply. By including gold in a portfolio, investors reduce the negative impact of inflation on their overall wealth. Its ability to maintain purchasing power makes it a critical tool in wealth preservation strategies. Physical gold is tangible, culturally significant, and emotionally valued, especially in countries like India. However, it comes with higher costs such as making charges for jewellery, storage, and insurance. Digital gold and Gold ETFs provide easier access and trading convenience, often at lower costs. ETFs can be traded on stock exchanges, giving flexibility, while digital gold can be purchased in micro amounts through apps. The choice depends on your investment goals, risk tolerance, and whether you prioritize convenience or traditional ownership. Yes, gold prices are influenced by global economic and geopolitical factors. A strong US dollar often reduces gold prices, while a weaker dollar can push them higher. Interest rate changes, inflation expectations, and central bank policies also significantly affect gold demand and pricing. Additionally, geopolitical tensions, wars, and financial crises increase investor demand for gold as a safe-haven asset. Global supply and demand dynamics, including mining output and investor sentiment, further impact its market price. Understanding these factors helps investors make informed decisions about timing and allocation. Gold generally does not outperform stocks or mutual funds over the long term in terms of wealth creation. Stocks and mutual funds offer higher growth potential through capital appreciation and dividends, making them better for aggressive long-term wealth building. Gold’s primary advantage is stability and safety, especially during market downturns or economic uncertainty. By including gold in a portfolio, investors can reduce overall volatility and protect against financial risks. It is best used as a hedge or complementary asset rather than the main growth driver. Yes, Sovereign Gold Bonds (SGBs) are considered one of the safest ways to invest in gold. They are issued and backed by the Government of India, eliminating the risk of theft or market manipulation associated with physical gold. SGBs offer 2.5% annual interest on the invested amount in addition to capital gains from gold price appreciation. They also provide tax benefits if held until maturity, including exemption from capital gains tax. SGBs are suitable for long-term investors who want secure returns with additional income. The best time to invest in gold is during periods of inflation, global uncertainty, or geopolitical tensions. Gold acts as a safe-haven asset when markets are volatile or currencies weaken. Long-term investors can also benefit by investing regularly through small allocations, regardless of short-term price fluctuations. Timing the market is less important than maintaining consistent exposure to hedge against future risks. Gold performs best as part of a diversified portfolio rather than as the sole investment, providing stability and peace of mind.3. Advantages of Investing in Gold

3.1 Hedge Against Inflation

Why gold hedges inflation

Condition

Currency Impact

Gold Effect

High inflation

Value falls

Price rises

Weak Rupee

Savings erode

Gold gains

Cost of living rise

Loss grows

Hedge works

3.2 High Liquidity

Liquidity benefits

3.3 Portfolio Diversification

Asset Type

Nature

Risk Level

Correlation with Gold

Equity

Growth asset

High

Low correlation

Bonds

Fixed income

Low

Medium correlation

Real estate

Physical asset

Moderate

Low correlation

Gold

Hedge asset

Low

Negative correlation

Why gold improves balance

3.4 Safe-Haven Asset

When gold becomes safe haven

Situation

Risk Level

Gold Behaviour

War fears

Extreme

Prices rise

Global recession

High

Demand spikes

Stock crash

High

Stability improves

Policy fear

Moderate

Hedge increases

Summary of Gold Benefits

Advantage

Key Benefit

Inflation Hedge

Protects purchasing power

Liquidity

Easy buying and selling

Diversification

Reduces total risk

Safe Haven

Works during crises

4. Risks & Limitations of Gold Investment

4.1 No Regular Income

Why this matters

Asset Type

Gives Income?

Example

Gold

No

Physical, ETF

Stocks

Yes

Dividends

FD

Yes

Fixed interest

Real estate

Yes

Rent

4.2 Short-Term Price Volatility

Causes of volatility

Duration

Movement

Risk

Short term

High

Volatile

Medium term

Moderate

Manageable

Long term

Stable

Strong

4.3 Storage and Extra Charges

Extra costs in physical gold

Type

Hidden Cost

Impact

Jewellery

Making charge

Lower resale

Coins/Bars

Storage cost

Extra expense

Digital

No storage cost

Easier holding

4.4 Global Influence on Prices

Key price influencers

Factor

Gold Impact

Strong dollar

Price weakens

Weak dollar

Price rises

High rates

Demand reduces

Crisis fear

Demand increases

Summary of Gold Limitations

Limitation

Impact

No income

Slower returns

Volatility

Short-term risk

Storage charges

Lower profit

Global influence

Price uncertainty

5. Ways to Invest in Gold

5.1 Physical Gold

Pros

Cons

Type

Use Case

Limitation

Jewellery

Cultural use

High charges

Coins

Savings purpose

Storage needed

Bars

Bulk investment

Resale difficulty

5.2 Gold ETFs & Gold Mutual Funds

Feature

ETF

Gold Fund

Storage

No

No

Liquidity

High

Moderate

Demat Needed

Yes

No

Pricing

Market-linked

NAV-linked

5.3 Sovereign Gold Bonds (SGBs)

Benefits of SGBs

Feature

SGB Benefit

Safety

Government backed

Return

Interest + growth

Storage

None required

Taxation

Maturity exempt

5.4 Digital Gold

Pros

Cons

Comparison Table of Gold Investment Options

Option

Storage Need

Liquidity

Extra Benefit

Suitability

Physical

Yes

Medium

Tangible asset

Traditional buyers

ETF

No

High

Market access

Active traders

Gold Fund

No

Medium

No Demat needed

New investors

SGB

No

Low-Medium

Interest income

Long-term holders

Digital

No

High

Small ticket size

Beginners

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

6. When Does Gold Work Best as an Investment?

6.1 During Inflationary Cycles

Why it helps in inflation

Situation

Currency Effect

Gold Result

High inflation

Value drops

Price climbs

Weak Rupee

Savings shrink

Hedge strengthens

Commodity rise

Costs soar

Gold benefits

6.2 During Global Uncertainty

Events that boost gold demand

Event Type

Market Impact

Gold Behaviour

War fears

Panic rises

Price increases

Recession talk

Growth weakens

Gold stabilizes

Banking stress

Trust falls

Gold gains

Policy shocks

Volatility rises

Demand grows

6.3 As a Portfolio Allocation

Ideal usage strategy

Allocation Range

Investor Type

Benefit

5%

Conservative

Backup security

10%

Balanced

Risk reduction

15%

Cautious

Crisis protection

Key Points

Condition

Gold Performance

Inflation

Strong

Uncertainty

Strong

Stability

Moderate

Long-term

Reliable

7. Gold vs Other Investments

7.1 Gold vs Stocks

Factor

Gold

Stocks

Return

Moderate

High

Risk

Low

High

Income

None

Dividends

Growth

Slow

Strong

7.2 Gold vs Real Estate

Factor

Gold

Real Estate

Liquidity

High

Low

Income

None

Rent possible

Entry cost

Low

Very high

Maintenance

None

High

7.3 Gold vs Fixed Deposits

Factor

Gold

FD

Income

None

Yes

Risk

Low

Very low

Inflation hedge

Strong

Weak

Liquidity

High

Medium

7.4 Gold vs Mutual Funds

Gold suits risk balancing purpose.

Factor

Gold

Mutual Fund

Purpose

Safety

Growth

Volatility

Moderate

Market-linked

Return

Steady

Compounding

Usage

Hedge

Wealth creation

7.5 Where Gold Fits

Quick Summary Table

Investment Type

Primary Benefit

Limitation

Best For

Gold

Stability

No income

Safety hedge

Stocks

Growth

High risk

Long-term gain

Real Estate

Asset building

Low liquidity

Wealth build

FD

Guaranteed return

Low return

Safe income

Mutual Funds

Compounding

Market swings

Long-term goals

8. Conclusion

Gold Rate in Kerala Today

The Ultimate Guide to Personal Finance in India

Electronic Gold Receipts (EGR): What It Is, How It Works & Why It Matters for Investors

Stock Market Training Reviewed & Monitored by SEBI Registered Investment Advisor

Frequently Asked Questions

Is gold a safe investment?

How much gold should I hold in my portfolio?

Does gold give regular income?

What are the best ways to invest in gold?

How does gold protect against inflation?

Is physical gold better than digital gold or ETFs?

Do global factors affect gold prices?

Can gold outperform stocks or mutual funds?

Are Sovereign Gold Bonds safe?

When is the best time to invest in gold?

{kind=link}